You're standing at a crossroads that millions of Americans face every year, but this time it's personal. The decision between buying and renting a home in Chestnut Ridge isn't just about monthly payments or square footage. It's about your lifestyle, your dreams, your financial future, and the kind of life you want to build for yourself and your family.

As someone who has spent years analyzing real estate markets and helping families make this exact decision, I can tell you that there's no one-size-fits-all answer. But there is a right answer for you, and by the end of this guide, you'll have the clarity and confidence to make it.

Buying vs. Renting in Chestnut Ridge: What We’ll Cover

- Why Chestnut Ridge Has Everyone Talking

- The Emotional Reality of Buying

- The Renting Reality

- Buying vs. Renting Comparison

- Making the Decision

- FAQ

Why Chestnut Ridge Has Everyone Talking

Let's start with why you're even considering Chestnut Ridge. This isn't just another suburb. It's a community that has mastered the art of balance, offering the tranquility of suburban living while keeping Manhattan just 30 miles away. When you drive through these tree-lined streets, you immediately understand why families are flocking here.

The numbers tell a compelling story. Home values have surged 15.5% in just one year, reaching a median price of $950,000. That might make you gulp, but it also signals something important: this is a community where people want to be, and that demand creates both opportunities and challenges depending on which side of the buy-versus-rent equation you're on.

With 77% of residents owning their homes and 23% renting, Chestnut Ridge has created a stable community where neighbors know each other's names and kids can safely ride their bikes to the local park. The median rent of $2,093 per month reflects the quality of life here, but it also represents a significant monthly commitment that deserves careful consideration.

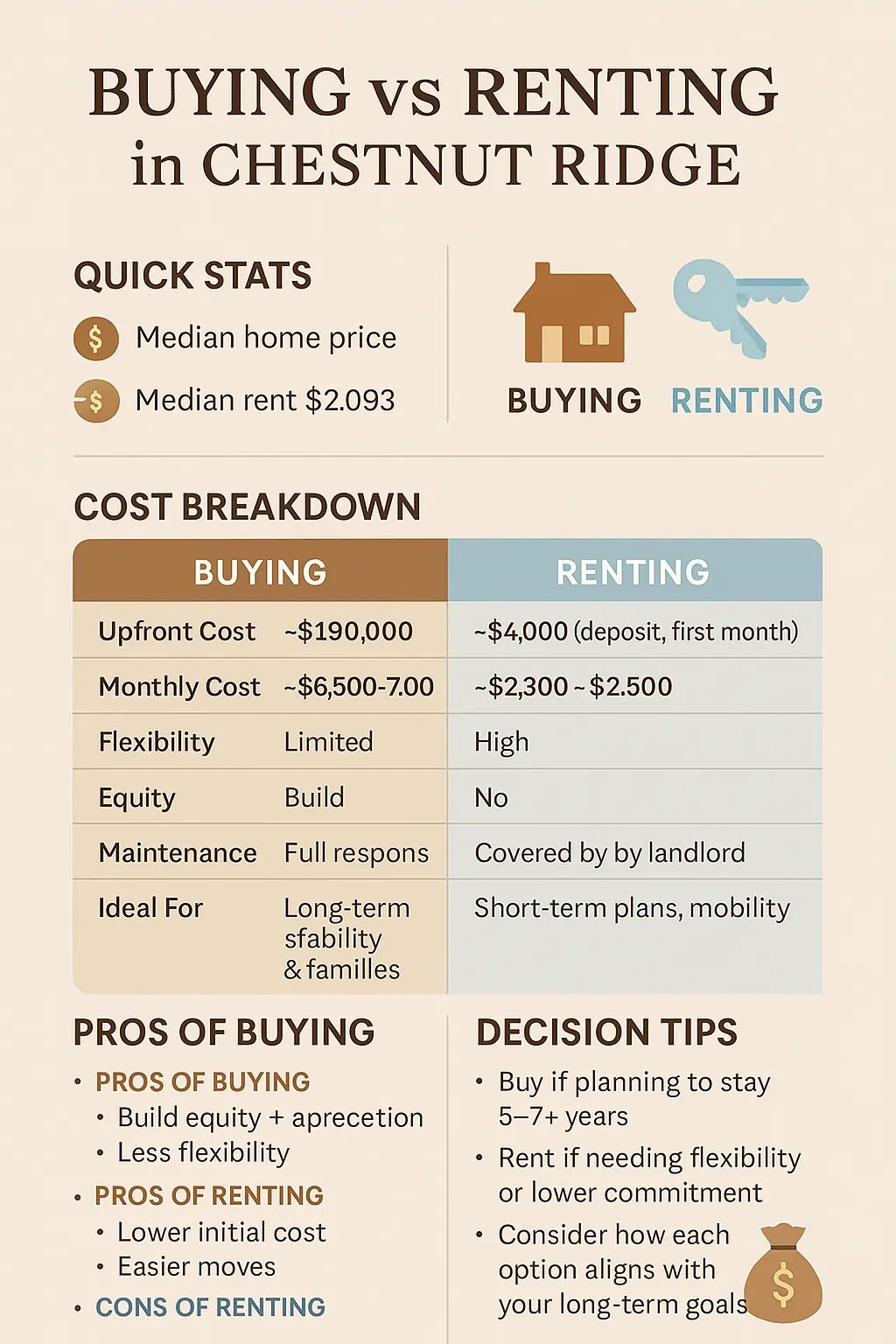

Category 🏡 Buying a Home 🛋️ Renting a Home Upfront Cost High – Around $190,000 (20% down + closing costs) Low – Typically $4,000–$5,000 (deposit + first month) Monthly Cost $6,500–$7,000 (includes mortgage, taxes, insurance, upkeep) $2,300–$2,500 (rent + utilities + insurance) Equity Building ✅ Yes – Builds wealth through appreciation ❌ No – Monthly rent doesn't build ownership Flexibility ❌ Low – Harder to relocate or resize on short notice ✅ High – Easy to move or downsize as needed Tax Benefits ✅ Available – Mortgage interest & property tax deductions ❌ None – No tax incentives Maintenance Responsibility ❌ Full – Homeowner handles all repairs and upkeep ✅ Minimal – Covered by landlord/property manager Lifestyle Customization ✅ Full Control – Renovate and personalize freely ❌ Limited – Lease restrictions apply Risk Exposure ⚠️ Higher – Market fluctuations, repair surprises ⚠️ Moderate – Rent increases, non-renewal risk Best For 👪 Long-term stability, families, wealth building 👤 Short-term plans, job moves, flexibility seekers Amenities Access ❌ Extra Cost – Must install (e.g., pool, gym) ✅ Included – Often part of rental communities

The Renting Reality: Freedom with a Different Kind of Security

Renting often gets unfairly characterized as "throwing money away," but that's a oversimplification that ignores the very real benefits that make renting the right choice for many smart, successful people.

Flexibility as a Superpower

In today's economy, flexibility isn't just nice to have; it's often essential for career advancement and personal growth. If an amazing job opportunity arises across the country, renters can take advantage without the stress and expense of selling a home in a potentially unfavorable market.

This flexibility extends beyond career moves. Maybe you want to try living closer to downtown after a few years in the suburbs. Perhaps your family size changes and your space needs shift dramatically. Renters can adapt to life's changes more easily than homeowners who are anchored by mortgage commitments and transaction costs.

Lower Financial Barriers and Different Investment Opportunities

The typical renter in Chestnut Ridge needs to come up with a security deposit and first month's rent, perhaps $4,000 to $5,000 total. Compare that to the nearly $200,000 needed for a down payment on a median-priced home, and you can see why renting makes financial sense for many people.

This lower barrier to entry means renters can potentially invest the money they would have used for a down payment in other assets: stocks, bonds, or even starting a business. While homeowners build equity in real estate, smart renters can build wealth through diversified investments that might actually outperform the housing market.

Maintenance-Free Living

There's genuine peace of mind in knowing that when something breaks, it's not your problem to solve or pay for. This isn't just about money; it's about time and stress. Many rental communities in Chestnut Ridge offer amenities like fitness centers, pools, and social spaces that would cost homeowners tens of thousands of dollars to install and maintain.

The Challenges Renters Face

The biggest psychological challenge for renters is the feeling that they're not building toward anything permanent. Every month, $2,093 goes to rent, and while you get the benefit of housing, you don't get any ownership stake. In a appreciating market like Chestnut Ridge, this can feel particularly painful as you watch home values climb while your rent payments simply disappear.

Rent increases are another reality. While Chestnut Ridge has seen modest increases of 1.6% annually, there's no guarantee this will continue. A new property management company or changes in the local market could result in more significant increases that strain your budget.

Limited personalization options can also be frustrating. Most leases restrict major changes, so you might live with outdated fixtures, paint colors you dislike, or layouts that don't quite work for your lifestyle.

🏠 Buying vs Renting in Chestnut Ridge: A Side-by-Side Breakdown

The Financial Deep Dive: Crunching Numbers That Matter

Let's get specific about what these choices mean for your wallet, both immediately and over time.

The True Cost of Buying

A $950,000 home with a 20% down payment leaves you with a $760,000 mortgage. At current interest rates around 6.9%, your monthly principal and interest payment would be approximately $5,010. Add property taxes, insurance, PMI (if you put down less than 20%), and maintenance, and you're looking at a total monthly cost of around $6,500 to $7,000.

But here's what the payment calculators don't tell you: in the early years of your mortgage, most of that payment goes to interest, not principal. You're building equity slowly at first, with the pace accelerating over time.

The Renting Reality Check

At $2,093 per month for rent, plus utilities and renter's insurance, a typical renter might spend $2,300 to $2,500 monthly for housing. That's significantly less than the buying scenario, but remember that none of this builds equity.

However, if a renter invests the difference between renting and owning costs ($4,000 to $4,500 monthly) in diversified investments earning 7% annually, they could potentially build significant wealth over time. The key word is "if" because it requires discipline that many people struggle to maintain.

The Break-Even Analysis

Generally, buying makes more financial sense if you plan to stay in the same home for at least five to seven years. This timeframe allows you to recoup the transaction costs of buying and potentially benefit from appreciation. If you might move sooner, renting often makes more financial sense.

Lifestyle Considerations That Numbers Can't Capture

Beyond the financial calculations, your housing choice profoundly impacts how you live day to day.

Space and Privacy

Chestnut Ridge homes typically offer more space than rental units, including private outdoor areas where kids can play and adults can entertain. This extra space becomes invaluable for families or anyone who works from home.

Community Integration

Homeowners tend to be more invested in local schools, community organizations, and neighborhood issues. If being deeply rooted in your community matters to you, ownership often facilitates this better than renting.

Lifestyle Flexibility

Renters often have access to amenities that would be prohibitively expensive for individual homeowners: pools, fitness centers, social spaces, and professional landscaping. If you value these amenities but don't want the responsibility of maintaining them, renting might align better with your lifestyle preferences.

Making the Decision: A Framework for Your Situation

Here's a practical framework to help you decide what makes sense for your unique situation:

Choose Buying If:

- You plan to stay in Chestnut Ridge for at least five to seven years

- You have stable income and substantial savings for down payment and emergencies

- You value the ability to customize your living space

- Building equity and potential appreciation appeal to you

- You want deeper community roots and stability

- You're comfortable with maintenance responsibilities and unexpected costs

Choose Renting If:

- Your career or life situation might require flexibility in the next few years

- You prefer to invest your money in assets other than real estate

- You want access to amenities without maintenance responsibilities

- You're new to the area and want to explore different neighborhoods

- The upfront costs of buying would strain your finances

- You prefer predictable monthly expenses without surprise repair bills

Advanced Strategies and Considerations

For Potential Buyers:

Consider house hacking opportunities, where you buy a duplex or home with a rental unit to help offset mortgage costs. Some buyers in Chestnut Ridge have successfully purchased properties with accessory dwelling units or basement apartments that generate rental income.

Explore different loan programs beyond conventional mortgages. FHA loans require smaller down payments, and some local programs offer assistance for first-time buyers or essential workers.

Think about timing strategically. While trying to time the market perfectly is impossible, understanding seasonal patterns and local market conditions can help you make a more informed decision.

For Potential Renters:

Negotiate lease terms beyond just rent. Some landlords will agree to longer lease terms in exchange for modest rent reductions or improvement allowances.

Consider renting in newer communities that offer more amenities and potentially more stable management.

Create a dedicated investment strategy for the money you're not putting into a home purchase. Automatic investments can help ensure you actually build wealth rather than simply spending the difference.

The Hidden Factors That Influence Your Decision

Tax Implications

Homeowners can deduct mortgage interest and property taxes, which can provide significant tax benefits, especially in the early years of ownership when interest payments are highest. However, recent changes to tax laws have reduced these benefits for some taxpayers.

Renters don't receive direct tax benefits from their housing costs, but they also don't face the risk of property tax increases or special assessments.

Insurance Considerations

Homeowners need more comprehensive insurance coverage, including dwelling, personal property, and liability protection. These costs can add $200 to $400 monthly to homeownership expenses.

Renters need only personal property and liability coverage, typically costing $15 to $30 monthly, though they should verify that their landlord's insurance adequately protects the building structure.

Market Timing Reality

While you shouldn't try to time the market perfectly, understanding current conditions helps inform your decision. Chestnut Ridge's 15.5% appreciation in one year suggests a hot market where buyers might face bidding wars and compressed timelines.

In such markets, buyers often waive inspections or offer above asking price, increasing both costs and risks. Renters might find fewer available units but also more negotiating power if landlords are competing for quality tenants.

FAQ: Addressing Real Concerns

Q: What if I can't afford a 20% down payment in Chestnut Ridge?

A: You have several options. FHA loans allow down payments as low as 3.5%, though you'll pay mortgage insurance. Some conventional loans accept down payments as low as 3% for qualified buyers. VA loans (for eligible veterans) and USDA loans (for qualified rural areas) offer zero-down options. Additionally, some employers and local organizations offer down payment assistance programs.

Q: How do I know if a rental property is fairly priced in Chestnut Ridge?

A: Research comparable rentals using websites like Zillow, Apartments.com, and local rental listings. Consider the total value package: amenities, location, property condition, and included utilities. A slightly higher rent might be justified by superior amenities or a prime location near schools or transportation.

Q: What's the real cost difference between buying and renting over 10 years?

A: This depends heavily on market performance, but here's a general framework: Over 10 years, a buyer builds significant equity through principal payments and potential appreciation. However, they also pay substantial interest, taxes, insurance, and maintenance costs. A renter pays only for housing costs but builds no equity. The outcome depends on home appreciation rates versus investment returns on the money not tied up in real estate.

Q: Should I wait for the market to cool down before buying?

A: Market timing is notoriously difficult and often counterproductive. If you're financially ready, plan to stay long-term, and find a home you love at a price you can afford, current market conditions shouldn't deter you. Remember, you can refinance if rates improve, but you can't go back and buy at yesterday's prices.

Q: What are the biggest mistakes first-time buyers make in Chestnut Ridge?

A: Common mistakes include: underestimating total monthly costs beyond the mortgage payment, not getting pre-approved before house hunting, waiving inspections in competitive markets, not budgeting for immediate repairs and improvements, and buying the most expensive home they qualify for rather than what they can comfortably afford.

Q: How do I evaluate rental communities versus individual rental homes?

A: Consider your priorities: rental communities often offer amenities, professional management, and social opportunities but may feel less personal. Individual homes typically provide more space and privacy but depend heavily on individual landlord quality. Evaluate maintenance responsiveness, lease terms, pet policies, and overall value for your specific needs.

Q: What questions should I ask landlords or property managers?

A: Key questions include: What's included in rent? How are maintenance requests handled? What's the typical timeline for repairs? Are there additional fees beyond rent and security deposit? What's the pet policy? How much notice is required for lease non-renewal? Can I make minor modifications like painting? What's the guest policy?

Q: How do property taxes work in Chestnut Ridge, and will they increase?

A: Property taxes fund local services like schools, police, and infrastructure. They're based on assessed property value and local tax rates. While rates can change, dramatic increases are relatively rare and usually occur gradually. When evaluating a purchase, factor in potential tax increases over time, especially if you're buying during a period of rapid appreciation.

Q: Is buying a fixer-upper a good strategy in Chestnut Ridge?

A: Fixer-uppers can offer value opportunities but require careful evaluation. Consider your renovation skills, available time, and budget for improvements. In a hot market like Chestnut Ridge, competition for fixer-uppers can be intense, and renovation costs often exceed initial estimates. Only pursue this strategy if you have substantial reserves and realistic timelines.

Q: How do I protect myself from rental scams?

A: Red flags include requests for money before viewing the property, prices significantly below market rate, landlords who can't meet in person, and pressure to sign leases immediately. Always verify ownership, visit properties in person, research the landlord or management company, and never wire money or provide bank account information until you've thoroughly vetted the opportunity.

Your Next Steps: Moving from Decision to Action

Once you've weighed all these factors and decided which path aligns with your goals, here's how to move forward effectively:

If You're Buying:

- Get pre-approved with multiple lenders to understand your true buying power and secure the best rates

- Find a buyer's agent who knows Chestnut Ridge intimately and can guide you through competitive situations

- Establish your maximum budget including all costs, not just the purchase price

- Prepare for a competitive market by having all documentation ready and being flexible on timelines

- Budget for immediate move-in costs, improvements, and an emergency fund for unexpected issues

If You're Renting:

- Define your must-haves versus nice-to-haves in terms of location, amenities, and space

- Prepare a rental application package with references, income verification, and credit reports

- Research landlords and management companies before applying

- Understand lease terms completely before signing

- Create an investment plan for the money you're not putting into homeownership

The Bottom Line: Your Housing Choice Shapes Your Life

The decision between buying and renting in Chestnut Ridge isn't just about money, though financial considerations are crucial. It's about the kind of life you want to live, the risks you're comfortable taking, and the dreams you're working toward.

Homeownership in Chestnut Ridge offers the potential for wealth building, stability, and the deep satisfaction of creating a space that's truly yours. But it also requires significant financial resources, comfort with risk, and acceptance of ongoing responsibilities.

Renting provides flexibility, lower upfront costs, and freedom from maintenance hassles. But it also means missing out on potential appreciation and the psychological benefits of ownership.

Both choices can be smart, depending on your circumstances, goals, and priorities. The key is making a decision that aligns with your values and supports the life you want to build.

Chestnut Ridge is a special community that offers quality of life regardless of whether you rent or own. Focus on making the choice that positions you for long-term success and happiness, knowing that both paths can lead to a fulfilling life in this exceptional place.

Remember, this decision isn't permanent. Many people rent first to get to know an area, then buy when they're ready. Others sell homes to gain flexibility during life transitions. What matters most is making the choice that's right for you today, with the information and resources you have available.

Whatever you decide, Chestnut Ridge offers the quality of life, community spirit, and growth potential that make it an excellent place to call home. The question isn't whether Chestnut Ridge is right for you; it's which way of living here will help you thrive.