Is a Co-op Better Than a Condo in NYC? The Decision That Will Shape Your Future

You're ready to buy a home in NYC—but should it be a co-op or a condo? For most New Yorkers, this decision is a make-or-break moment that can shape their financial future and lifestyle for years. In 2025, with shifting market dynamics and evolving buyer priorities, making the right choice between a co-op or condo has never been more critical.

"I nearly made a $150,000 mistake by not understanding the true differences," shares Michael, a first-time NYC homebuyer who almost signed a contract before realizing the implications. "What seemed like minor details turned out to be game-changers for my situation."

As a team with over 25 years of combined experience in NYC real estate, we've guided hundreds of buyers through this exact decision—and we've seen both the success stories and the costly mistakes. Let's cut through the confusion to help you make the choice that's right for your unique situation.

What's the Difference Between a Co-op and Condo in NYC?

Before diving into the details, understand this fundamental NYC reality: co-ops represent roughly 75% of Manhattan's housing stock—though only about 25% of available listings at any given time. This discrepancy exists because co-op owners typically stay put longer, while condos change hands more frequently.

Ownership Structure: What You're Actually Buying

Co-op Ownership:

- Shares in a corporation that owns the building

- Proprietary lease granting you the right to live in a specific unit

- Like buying stock in a company where your "dividend" is a place to live

- Board has significant control over who buys and sells

Condo Ownership:

- Direct ownership of the actual apartment (walls, floors, windows)

- Deed to your specific unit, just like a house

- Ownership percentage in common areas

- Significantly less board control over buying and selling

Sarah, who purchased her Upper West Side co-op in 2024, explains: "Understanding that I wasn't buying real estate, but rather shares in a corporation, completely changed my perspective on what rights I actually had."

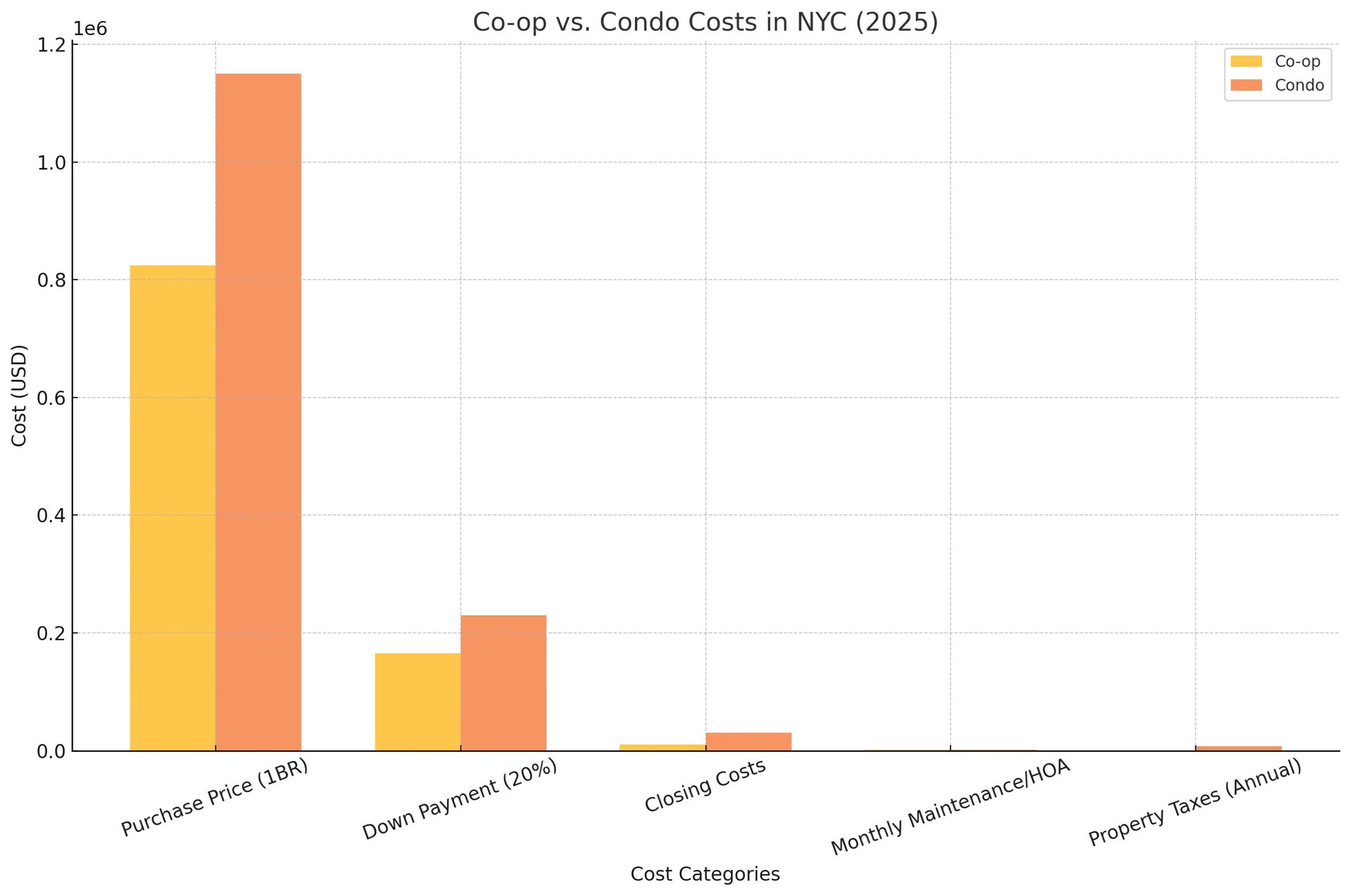

Co-op vs. Condo: The Financial Breakdown (2025)

Purchase Price: How Much Do Co-ops and Condos Cost in NYC?

The price gap between co-ops and condos has widened in 2025:

Co-op median price: $825,000 (Manhattan) Condo median price: $1,150,000 (Manhattan)

That's a 28% difference—translating to hundreds of thousands in potential savings for co-op buyers. For the same budget, most buyers can get 20-30% more space in a co-op compared to a condo in the same neighborhood.

Down Payment Requirements: The Cash You'll Need Upfront

This is where co-ops show their demanding side:

Co-ops typically require:

- 20-50% down payment

- Strong debt-to-income ratio (housing costs under 25-30% of gross income)

- Liquid assets equivalent to 1-2 years of mortgage and maintenance

Condos will accept:

- As little as 10% down

- More flexible financial requirements

- Less scrutiny of your overall financial picture

"For a $1 million apartment, that's the difference between needing $200,000-$500,000 cash for a co-op versus just $100,000 for a condo," explains Elena Rodriguez, a veteran NYC mortgage broker.

Monthly Costs: What You'll Pay After Closing

Here's where the numbers get interesting:

Co-op monthly costs:

- Maintenance fees (typically includes property taxes)

- Average: $1,750/month for a 1-bedroom

Condo monthly costs:

- Common charges + separate property taxes

- Average: $1,400 common charges + $600 property taxes = $2,000/month

"Many buyers fixate on the lower common charges without understanding the total monthly outlay," notes financial advisor Marcus Williams. "When you calculate the complete picture, co-ops can sometimes be more affordable long-term."

Closing Costs: Hidden Savings

Co-ops offer significant savings at closing:

- No mortgage recording tax (saves about 1.8-1.925% of your loan amount)

- No title insurance (saves roughly 0.4-0.5% of purchase price)

On a $1 million purchase with 80% financing, these savings could amount to $15,000-$20,000.

The True Cost of Ownership: A Real-World Comparison

Let's break down what this looks like in practice with a sample calculation comparing similar apartments:

Co-op True Cost:

- Purchase price: $800,000

- Down payment (30%): $240,000

- Monthly mortgage payment (4.75%, 30-year): $2,925

- Monthly maintenance: $1,750 (includes property taxes)

- Closing costs: Approximately $15,000

- First year total investment: $255,000 upfront + $56,100 annual carrying costs

Condo True Cost:

- Purchase price: $1,000,000

- Down payment (20%): $200,000

- Monthly mortgage payment (4.75%, 30-year): $4,170

- Monthly common charges: $1,400

- Monthly property taxes: $600

- Closing costs: Approximately $35,000

- First year total investment: $235,000 upfront + $74,040 annual carrying costs

"When you analyze the five-year cost of ownership including tax benefits and potential appreciation, most co-op owners save between $50,000-$100,000 compared to comparable condos," explains financial planner Jerome Hayes. "However, the initial financial barriers to entry can be significant."

How to Buy a Co-op vs. Condo: The Approval Process

Co-op Board Approval: The Financial Deep Dive

Co-op boards are infamous for their rigorous vetting process:

What to prepare:

- Tax returns (usually 2-3 years)

- Bank statements and investment accounts

- Credit reports and employment verification

- Debt-to-income documentation

- Proof of liquid assets (typically 1-2 years of payments after closing)

- Personal reference letters

- In-person board interview

"The co-op board approval process taught me more about my own finances than 15 years in banking," jokes Michael Chen, who purchased a Gramercy co-op last year.

The process typically takes 30-60 days after your offer is accepted, and boards can reject applicants without providing a reason.

Condo Approval: More of a Formality

By contrast, the condo purchase process is straightforward:

- Basic financial application

- Limited board review (primarily ensuring you're not violating building rules)

- No personal interview required

- Process typically takes just 2-3 weeks

Should I Buy a Co-op or Condo in NYC? Lifestyle Factors to Consider

Beyond finances, co-ops and condos create distinctly different living experiences.

Building Rules and Community

Co-op life means:

- Strict subletting policies (typically limited to 1-2 years, if permitted)

- Rigorous renovation approval processes

- Often stricter rules about pets, noise, and home businesses

- More owner-occupants and longer-term residents

- Stronger community ties and building events

Condo life offers:

- Liberal subletting rights (rent at will)

- More flexibility with renovations

- Generally more relaxed atmosphere

- Often more transient population

- Less community engagement but more privacy

"After living in both, I'd say co-ops feel more like a traditional neighborhood where everyone knows your business—for better or worse," shares Jessica, who moved from a Brooklyn Heights co-op to a Lower Manhattan condo in 2024.

Amenities and Building Features

The amenity gap remains substantial in 2025:

Condos typically feature:

- Rooftop lounges

- State-of-the-art fitness centers

- Pet spas and grooming stations

- Children's playrooms

- Co-working spaces

- Swimming pools

- Concierge services

Co-ops typically offer:

- More classic amenities like doormen

- Laundry rooms and storage

- Perhaps a modest gym or roof deck

- Larger apartment sizes and classic layouts

Best Co-op Buildings in NYC 2025: Neighborhood Considerations

Certain neighborhoods present particularly compelling opportunities for each housing type in 2025:

Best Co-op Values:

- Upper East Side (east of Third Avenue): Pre-war co-ops at 20-30% discounts

- Morningside Heights: Stately pre-war buildings with academic community feel

- Midtown East: Generous space and central location, often overlooked

- Jackson Heights (Queens): Garden co-ops with courtyards at a fraction of Manhattan prices

Best Condo Opportunities:

- Long Island City: Waterfront properties with Manhattan views

- Downtown Brooklyn: New developments with competitive pricing

- Hudson Yards/Far West Side: Increasing inventory creating buyer leverage

- South Harlem: New construction with growth potential

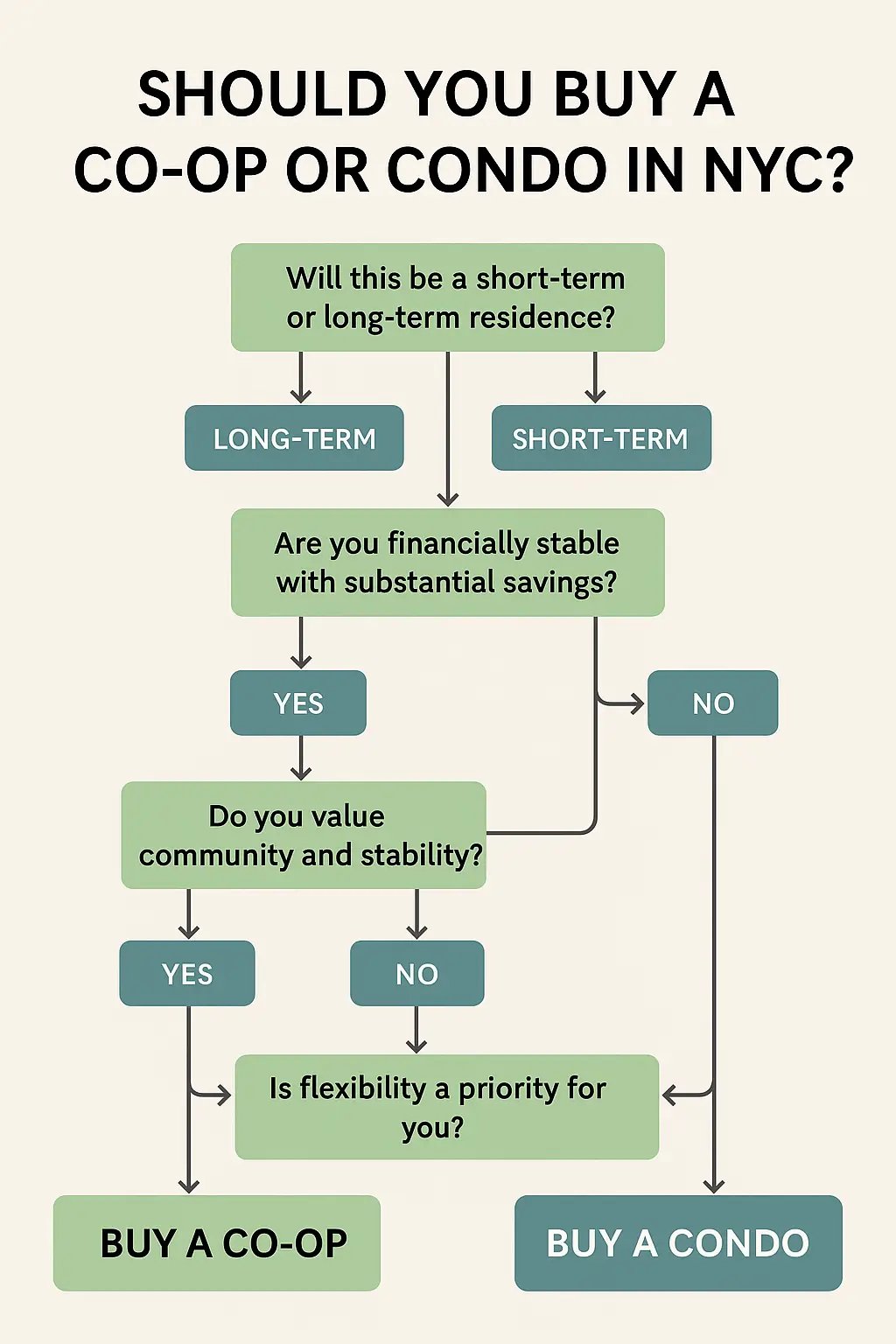

How to Choose: Co-op vs. Condo – 5-Step Decision Framework

After helping hundreds of New Yorkers navigate this critical decision, we've developed a proven 5-step framework to guide you to the right choice:

Step 1: Clarify Your Goals and Timeline

Ask yourself:

- Are you looking for long-term stability or maximum flexibility?

- How long will you realistically stay in this home?

- What matters more: price per square foot or ease of eventual selling?

"When I was honest about potentially relocating within three years, my decision became clear. The co-op savings weren't worth the potential hassle of getting board approval to sell or sublet later." — Miguel, finance professional who chose a condo

Step 2: Understand Your Complete Financial Picture

Calculate and compare:

- Total required upfront investment (down payment + closing costs)

- Monthly carrying costs (mortgage + maintenance/common charges + taxes)

- Long-term ownership costs (including tax benefits and potential assessments)

- Your financial qualification profile for each option

"Working with our financial advisor to create detailed 5-year projections of both options revealed that the co-op would cost us $87,000 less over five years, despite the higher down payment." — The Goldsteins, Upper West Side co-op owners

Step 3: Experience Both Options Firsthand

Make sure to:

- Visit multiple buildings of each type in your target neighborhoods

- Talk to current residents about their experiences

- Observe the atmosphere, amenities, and overall feel of different buildings

- Attend open houses during weekdays and weekends

"We were dead set on a condo until we visited a pre-war co-op with 11-foot ceilings and stunning original details. Sometimes you don't know what you value until you see it." — Leila, who switched from condo to co-op search

Step 4: Consult with NYC-Specialized Experts

Work with professionals who:

- Specialize in NYC's unique real estate market

- Have experience with both co-ops and condos

- Can provide neighborhood-specific insights

- Will be honest about your approval chances

"Our broker saved us from making a serious mistake. She identified three financial red flags that would have likely led to a co-op board rejection and steered us toward buildings with more suitable financial requirements." — James and Dana, first-time NYC buyers

Step 5: Trust Your Instincts

Remember that:

- Numbers matter, but so does how a place makes you feel

- Your specific needs may differ from market trends

- The "right" choice depends on your unique situation

- This is both a financial and lifestyle decision

"After all our research and spreadsheets, we ultimately chose the apartment where we could envision building our lives—the one that felt like home when we walked in." — Sarah and Michael, Battery Park City residents

Who Should Buy a Co-op in NYC? Is It Right for You?

Co-ops make the most sense if you:

- Value community and stability: "After three years in my co-op, I know all my neighbors by name. When I had surgery last year, five different neighbors offered to help with groceries and dog-walking." — Eliza, 41, healthcare professional

- Want more square footage for your money: "I was looking at 600-square-foot condo studios in Chelsea for $850K, then found a one-bedroom co-op with 800 square feet in the same neighborhood for $800K. The math wasn't complicated." — Jamie, 35, tech professional

- Have strong financial stability and savings: "The co-op board approval process seemed intimidating at first, but having our finances in order actually gave us confidence during the interview." — Mark and Leila, first-time buyers

- Plan to live in NYC long-term: "We knew we wanted to raise our family in this neighborhood for at least the next decade. The co-op's stable community and lower turnover were exactly what we wanted." — David, 38, educator

- Prefer classic architecture and larger floor plans: "My pre-war co-op has details you simply can't find in new construction—10-foot ceilings, herringbone floors, and rooms that feel properly proportioned." — Greta, 52, interior designer

Who Should Buy a Condo in NYC? Is It the Better Choice?

Condos are ideal if you:

- Want the freedom to rent out your property anytime: "I travel for work three months a year. Being able to Airbnb my place while I'm gone without board approval covers a significant portion of my mortgage." — Raj, 36, consultant

- Value modern amenities and luxury living: "After a long day, coming home to our building's spa, fitness center, and rooftop lounge feels like living in a resort. These amenities weren't negotiable for us." — Tyler and Christine, recent Manhattan transplants

- Need a simpler, faster purchase process: "I found my dream apartment and closed in 30 days. Friends buying co-ops were still waiting for board interviews when I was already moved in." — Lauren, 29, tech executive

- Have a strong income but less saved for a down payment: "With good credit and income but only 15% saved for a down payment, condos were our only realistic option in our target neighborhoods." — Alex, 33, marketing director

- Might relocate in the near future: "We weren't sure if we'd stay in NYC beyond 3-5 years. The condo gave us flexibility to sell quickly or rent out if we needed to move." — Jessica and Omar, 30s, finance professionals

Expert Advice: What Real Estate Professionals Want You to Know

We asked several top NYC real estate professionals for their most candid advice for 2025 buyers:

From a Real Estate Attorney: "The biggest mistake is falling in love with a co-op without understanding if you're financially qualified. Get a realistic assessment from an experienced broker before making an offer—co-op board rejections are emotionally and financially costly."

From a Mortgage Broker: "In 2025, with current interest rates, co-op buyers should scrutinize the building's financial health. Request multiple years of financial statements and have your attorney review them carefully. A well-funded reserve can save you thousands."

From a First-Time Homebuyer Specialist: "For most clients entering the market with budgets under $1 million, co-ops remain the only viable option in many neighborhoods. The key is finding buildings with reasonable financial requirements and subletting policies."

The Bottom Line: Making Your Decision

There's no universally "better" choice between co-ops and condos in NYC. The right decision depends entirely on your unique financial situation, lifestyle needs, and future plans.

In Manhattan's co-op-heavy market, eliminating co-ops from consideration means missing out on roughly 75% of potential homes. Conversely, focusing only on co-ops could mean sacrificing flexibility crucial to your future happiness.

The good news? In 2025's more balanced market, you have time to explore both options thoroughly before making this major financial decision. Whether you choose the community and value of a classic co-op or the flexibility and amenities of a modern condo, entering the decision fully informed is your best path to long-term satisfaction with your slice of New York City real estate.

Ready to Find Your Perfect NYC Home?

Our team of NYC real estate experts specializes in helping buyers navigate the co-op vs. condo decision across all five boroughs. With deep market knowledge and a personalized approach, we'll help you find the perfect match for your lifestyle and financial goals.

Contact us today for a free consultation and take the first step toward making the right choice for your NYC home purchase.

This guide was written by a team of NYC real estate experts with over 25 years of combined experience helping buyers navigate the unique challenges of New York City's housing market.