Does scrolling through NYC real estate listings feel like window shopping for designer clothes with empty pockets? Trust me, you're not alone. With the median Manhattan apartment price hovering around $1.2 million, the dream of homeownership in New York City can seem like just that—a dream.

But here's the good news: 2025 has ushered in a golden age of homebuyer assistance programs that are turning "someday" into "this year" for thousands of New Yorkers.

As someone who navigated this labyrinth myself (and helped dozens of clients do the same), I'm thrilled to share this insider's guide to the grants and programs that could save you tens of thousands on your journey to homeownership in the city that never sleeps.

Why Even the Most Skeptical New Yorkers Are Taking a Second Look at Buying

Let's be real - buying in NYC has always been tough. Between the 20% down payments (that's $240,000 on that median Manhattan apartment), co-op board approvals that feel like applying to an exclusive country club, and closing costs that could fund a luxury vacation, it's no wonder many New Yorkers resigned themselves to renting forever.

But the landscape is changing dramatically in 2025, thanks to expanded funding and new programs designed specifically for NYC's unique housing market.

"I never thought I'd own anything in this city," says Maria Gonzalez, a teacher who recently purchased a two-bedroom co-op in Jackson Heights with assistance from two of the programs we'll discuss. "The grants covered almost all of my down payment—I only needed to bring $8,000 to closing."

Stories like Maria's are becoming increasingly common as city and state officials recognize that homeownership is key to building intergenerational wealth and stabilizing neighborhoods.

The Most Powerful NYC Homebuyer Programs for 2025

Let's dive into the programs that are making the biggest impact this year. I've organized them by impact and accessibility, with insider tips on how to maximize your benefits.

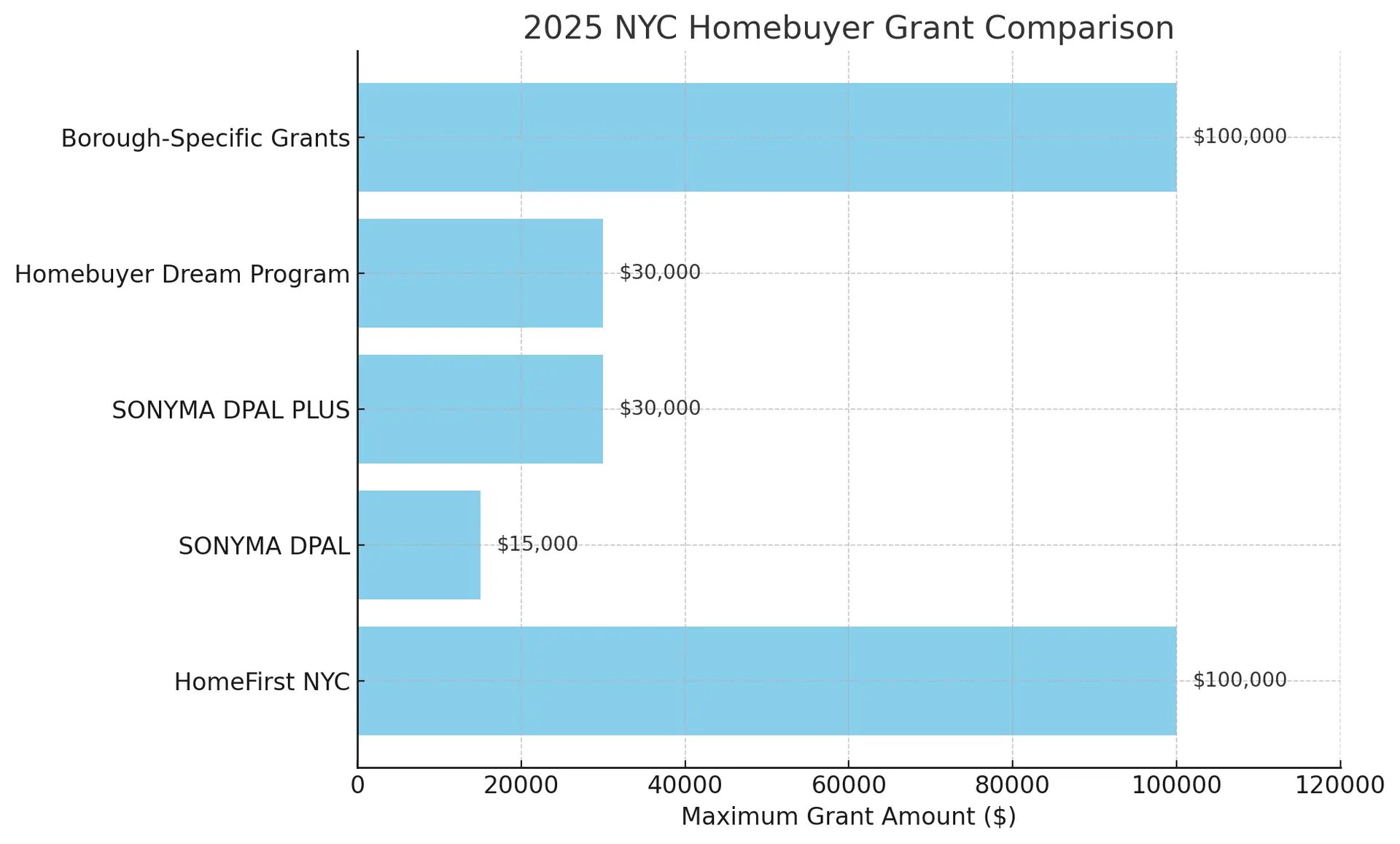

1. HomeFirst Down Payment Assistance: NYC's Game-Changing Program

Best for: First-time buyers who need significant help with down payment and closing costs

If there's one program to know about in 2025, it's HomeFirst. This NYC Department of Housing Preservation and Development (HPD) initiative has been supercharged with an $82 million investment, and the results are transformative.

What you get:

- Up to $100,000 for down payment or closing costs (yes, you read that right!)

- Available for 1-4 family homes, condos, or co-ops in any NYC borough

- Can be combined with certain other programs for even more savings

Who qualifies:

- First-time homebuyers (haven't owned residential property in the last three years)

- Household income up to 120% of Area Median Income ($124,400 for a family of four)

- Completion of a HUD-approved homebuyer education course

- Minimum contribution of 3% of the purchase price (can be gifted from family)

The fine print: You must live in the home for at least 10 years (for assistance up to $40,000) or 15 years (for assistance over $40,000). If you sell before then, you'll need to repay a portion of the assistance.

Insider tip: HomeFirst funds are allocated on a first-come, first-served basis. The moment you start thinking about buying, connect with a HomeFirst-approved counseling agency to get your application in the queue. Many buyers miss out simply because they apply too late in their home search.

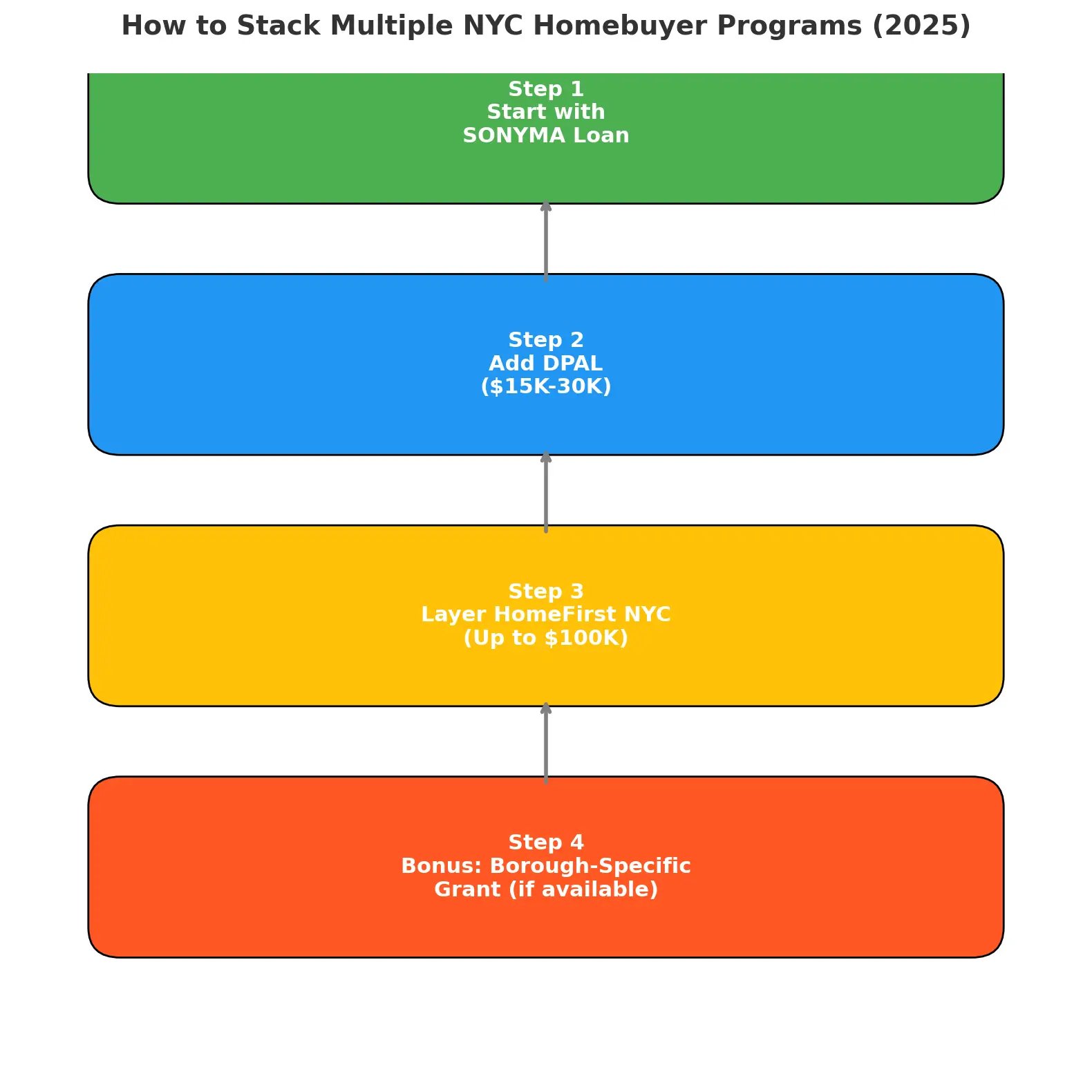

2. SONYMA: New York State's Suite of Buyer-Friendly Programs

Best for: Buyers who want flexible mortgage options with reduced interest rates and down payment assistance

The State of New York Mortgage Agency (SONYMA) offers a collection of programs that work beautifully for NYC buyers, especially when layered together.

A. Achieving the Dream

This flagship program is perfect for buyers stretching their budget to get into NYC's competitive market.

What you get:

- Down payments as low as 3% (compared to the 20% most NYC sellers expect)

- Below-market interest rates

- Available for 1-4 family homes, condos, co-ops, and even manufactured homes

B. Down Payment Assistance Loan (DPAL)

What you get:

- Up to $15,000 or 3% of the purchase price (whichever is higher) for down payment and closing costs

- 0% interest and no monthly payments

- Completely forgiven after 10 years if you stay in the home

C. DPAL PLUS ATD III (New for 2025!)

This enhanced program is designed for lower-income buyers who need even more help getting in the door.

What you get:

- Up to $30,000 for down payment and closing costs

- Can be used to cover mortgage insurance premiums

- Exclusively for households at or below 80% AMI

Who qualifies for SONYMA programs:

- First-time homebuyers (with some exceptions for veterans)

- Income and purchase price limits that vary by county (but are generous for NYC)

- Credit score typically 620 or higher

- Homebuyer education course completion

Real-world impact: Samantha, a graphic designer, used SONYMA's Achieving the Dream with DPAL to purchase a one-bedroom co-op in Astoria. "The lower down payment requirement meant I could buy three years earlier than I expected. And the DPAL essentially covered all my closing costs."

3. Homebuyer Dream Program: The Cherry on Top

Best for: Using alongside other programs for maximum assistance

This Federal Home Loan Bank of New York program provides grants up through member banks and credit unions.

What you get:

- Up to $30,000 for down payment and closing costs

- True grant money (not a loan)

- Can be combined with SONYMA and sometimes HomeFirst for maximum benefit

Who qualifies:

- First-time homebuyers

- Income up to 80% AMI

- Completion of homebuyer education

- Must apply through a participating lender

The catch: Funding is extremely limited and typically runs out early each year. For 2025, funds are available until November 28 or until depleted, whichever comes first.

Insider tip: Start talking to participating lenders in January or February, before the annual funding is announced. This puts you at the front of the line when applications open.

4. NYS HOME Program: Support for Lower-Income Buyers

Best for: Lower-income households and those buying in targeted revitalization areas

The NYS HOME Program uses federal funds distributed through local organizations to help expand homeownership opportunities.

What you get:

- Down payment and closing cost assistance (amounts vary by locality)

- Sometimes includes funds for necessary home repairs or renovations

- Often structured as a forgivable loan

Who qualifies:

- Income typically capped at 80% AMI

- First-time homebuyer status usually required

- Property must meet certain standards

- Requirements vary by administering organization

Why it matters: HOME funds often target neighborhoods undergoing revitalization, helping buyers who might otherwise be priced out due to gentrification.

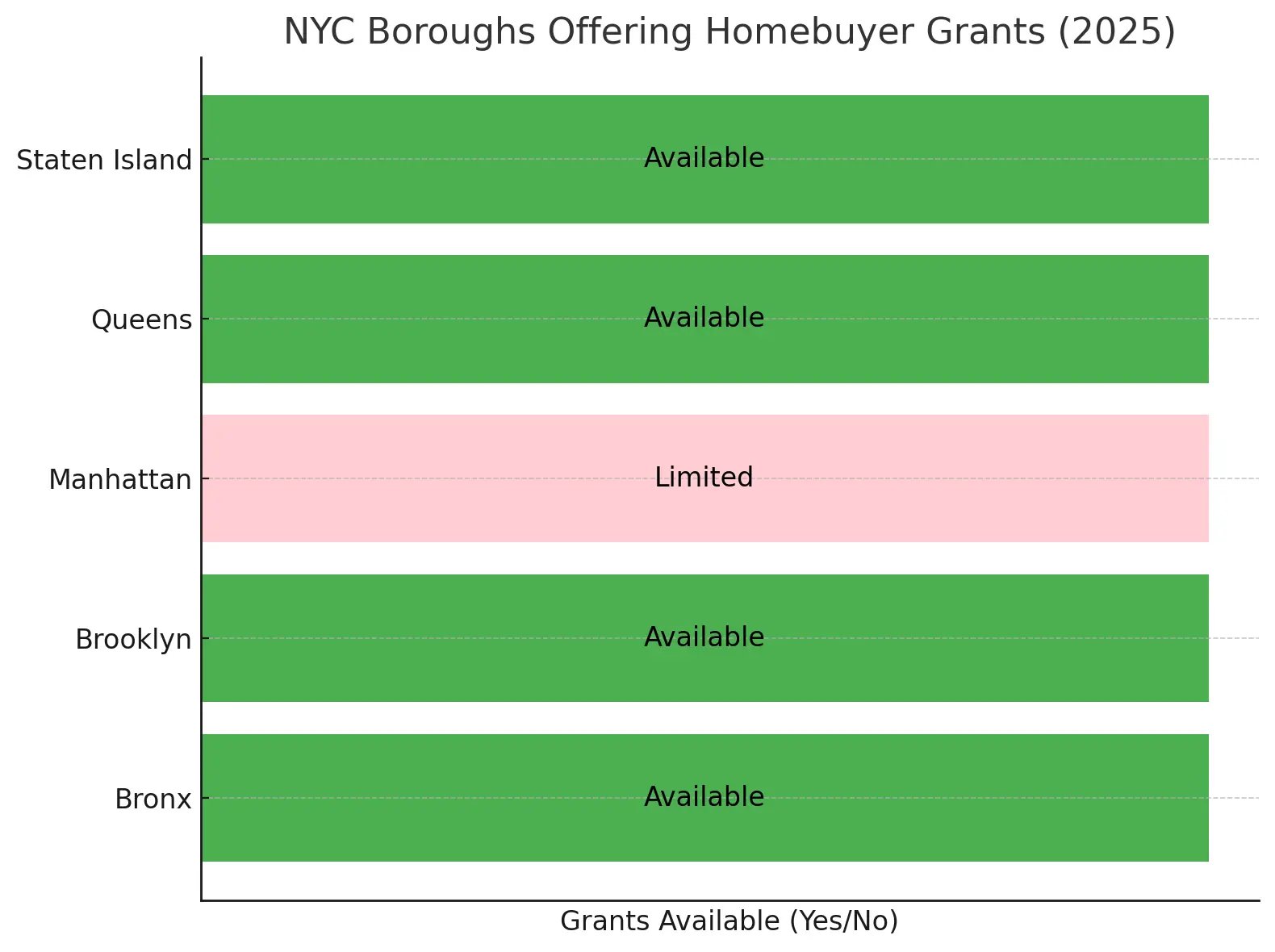

5. Borough-Specific Programs: Local Support for Your Dream

Best for: Those committed to buying in a specific borough or neighborhood

Some of NYC's most generous assistance comes from programs targeting specific boroughs or neighborhoods hoping to increase homeownership rates.

Examples for 2025:

- Staten Island HomeOwnership Initiative: Up to $100,000 in combined assistance

- Neighborhood Housing Services of Queens: Special down payment assistance for first-generation homebuyers

- Bronx Homeowners' Assistance Fund: Grants for down payment and repairs on older properties

Insider tip: These smaller programs often fly under the radar but can offer substantial help. Ask housing counselors specifically about borough initiatives early in your search.

Navigating the Application Process: Your Step-by-Step Guide

Getting approved for NYC homebuyer assistance isn't as complicated as you might think, but timing and preparation are everything.

Step 1: Education First

Almost every program requires completion of a homebuyer education course. Take this class before you start house hunting—it's not just a checkbox, but valuable preparation that will make you a more confident buyer.

Recommended providers:

- NHS of NYC (offers courses in all boroughs)

- AAFE (Asian Americans for Equality)

- Neighborhood Housing Services Brooklyn

- UNHP (University Neighborhood Housing Program) in the Bronx

Most courses cost $75-100 and can be completed online or in person over 1-2 days.

Step 2: Find a Housing Counselor Who Knows NYC

A good housing counselor is worth their weight in gold. They'll assess your financial situation, recommend specific programs, and guide your application process—usually for free.

Look for counselors certified by both HUD and the specific programs you're targeting (like HomeFirst or SONYMA).

Step 3: Get Your Documents in Order

Successful applicants are organized applicants. Create a digital folder with these documents, which you'll need for almost any assistance program:

- Last three years' tax returns (all pages)

- Six months of bank statements (all accounts)

- 30 days of pay stubs

- Gift letters (if family is helping)

- Credit reports from all three bureaus

- Proof of rent payments for the past year

- Photo ID and Social Security card

Step 4: Pre-Approval with a Program-Savvy Lender

Not all lenders understand NYC's unique assistance programs, particularly when it comes to co-ops (which make up approximately 75% of Manhattan's ownership market).

Work with a lender experienced in:

- SONYMA mortgages

- Co-op financing

- Combining multiple assistance programs

- NYC closing cost estimates

Pro tip: Ask potential lenders how many HomeFirst or SONYMA loans they've closed in the past year. If the answer is "just a few" or "none," keep looking.

Step 5: Submit Applications Early

For programs like HomeFirst with limited funding, submitting your application as early as possible is crucial. You don't need to have found a property yet—you can get conditionally approved while house hunting.

Common Questions About NYC Homebuyer Assistance

"Can I really combine multiple programs?"

Absolutely! The most successful buyers in NYC often layer 2-3 programs for maximum benefit. For example:

- SONYMA mortgage + DPAL + Homebuyer Dream Program

- HomeFirst + neighborhood-specific grant

- Employer assistance + SONYMA + borough program

Your housing counselor and lender will coordinate the logistics of using multiple programs together.

"Are there programs specifically for co-ops?"

While no major programs exclusively target co-ops, all the major assistance options (HomeFirst, SONYMA, etc.) can be used for co-op purchases. The challenge is finding co-op buildings that allow these programs.

Insider tip: When searching for co-ops, ask your agent to confirm the building is "SONYMA approved" and allows financing with less than 20% down. Not all do!

"How long does the approval process take?"

Plan for:

- Homebuyer education: 1-2 days

- Housing counseling: 2-4 weeks

- Program applications: 4-8 weeks

- Total: 2-3 months from start to conditional approval

Starting this process before you begin seriously house hunting will put you in a much stronger position when you find "the one."

"Do these programs affect what I can offer on a property?"

In competitive markets like Brooklyn and Manhattan, sellers sometimes prefer conventional buyers with 20% down over those using assistance programs. However, in 2025, this stigma is fading as these programs become more mainstream.

Solution: Have your lender write a strong pre-approval letter that focuses on your total qualification amount rather than detailing all funding sources. Then let your agent explain the reliability of your financing if questions arise.

Success Stories: Real New Yorkers, Real Homes

Michael & David: First-time buyers in Bedford-Stuyvesant Using HomeFirst ($80,000) + SONYMA with DPAL ($15,000) "We went from paying $3,200 in rent to a $2,900 mortgage payment—and now we own a two-bedroom in a neighborhood we love."

Asha: Single mom in Jamaica, Queens Using SONYMA + DPAL PLUS ($30,000) + employer assistance ($10,000) "I never thought I could afford to buy as a teacher and single parent. These programs changed everything for my daughter and me."

Carlos & Jessica: Young couple in the South Bronx Using HomeFirst ($60,000) + Bronx Homeowners' Assistance ($25,000) "We were able to buy and renovate a fixer-upper that's now worth $150,000 more than we paid. This created instant equity we never could have saved for otherwise."

Beyond the Purchase: Programs That Help You Stay Home

Getting the keys is just the beginning. These additional resources help ensure you can maintain your home for years to come:

- NYC Property Tax Relief for households earning under $200,000

- Home Energy Assistance Program (HEAP) for heating and cooling costs

- HomeFix for critical repairs after purchase

- Solar Homes Program for reduced energy costs

Your Action Plan: Next Steps Toward NYC Homeownership

- This week: Sign up for a homebuyer education course

- Next week: Schedule an appointment with a housing counselor

- Within 30 days: Gather your financial documents

- Within 60 days: Apply for specific programs based on your counselor's guidance

- Within 90 days: Begin working with a real estate agent who understands assistance programs

The Bottom Line: Is 2025 Your Year to Buy in NYC?

Despite the challenges, 2025 offers unprecedented support for aspiring NYC homeowners. With grants covering up to $100,000 of upfront costs, flexible mortgage options, and increasing inventory in many neighborhoods, this might be the year your dream becomes reality.

The catch? Many of these programs have limited funding that can run out by mid-year. Starting the process now—even if you're not ready to buy immediately—puts you in the best position to access these life-changing resources.

Need help navigating NYC's homebuyer assistance landscape? Request our free NYC Homebuyer Grants Checklist or schedule a consultation with a housing counselor specializing in first-time buyers.

This article is updated as of April 2025. Program details and availability may change. Always confirm current terms with official program administrators.