If you're a New York City property owner, you've probably already felt that familiar knot in your stomach when opening your latest property tax assessment. The numbers don't lie: NYC's fiscal year 2026 tentative assessment roll shows a staggering 5.7% city-wide property value increase, the largest jump we've seen in recent years.

But here's what the official reports won't tell you: this isn't just about numbers on a page. This is about real families, real budgets, and real financial stress.

In this guide, you'll learn:

- How the 5.7% NYC property tax hike impacts your wallet

- Borough-by-borough assessment breakdowns

- Step-by-step property tax appeal strategies

- Exemptions most people miss (and how to claim them)

- Tools to estimate your future tax bills

- A 30-day action plan to fight back effectively

As someone who has helped thousands of property owners navigate these treacherous waters over the past decade, I've seen firsthand how assessment increases can devastate household budgets overnight.

I've watched seniors on fixed incomes panic about losing their homes, young families struggle to absorb unexpected tax hikes, and small landlords face impossible choices between raising rents or operating at a loss.

But here's the good news: you're not powerless. With the right knowledge, strategies, and action plan, you can protect yourself and potentially save thousands of dollars. This guide will show you exactly how.

Table of Contents

- What the 5.7% Increase Really Means

- Borough-by-Borough Breakdown

- Hidden Costs of Higher Assessments

- How the Assessment Process Works

- 3-Phase Action Plan

- Exemptions You Might Be Missing

- Long-Term Protection Strategy

- Real Owner Case Studies

- Tools and Resources

- 30-Day Action Plan

- FAQs

What the 5.7% Increase Really Means {#what-the-57-increase-really-means}

When the NYC Department of Finance announced that total property values reached $1.579 trillion (a $85 billion increase from last year), it wasn't just celebrating robust economic recovery.

They were essentially announcing that millions of property owners would face higher tax bills, with many completely unprepared for the financial impact.

The taxable assessed value increased by 3.9% to $311.2 billion, but these percentages mask the real human cost. Let me break down what this means for different types of property owners:

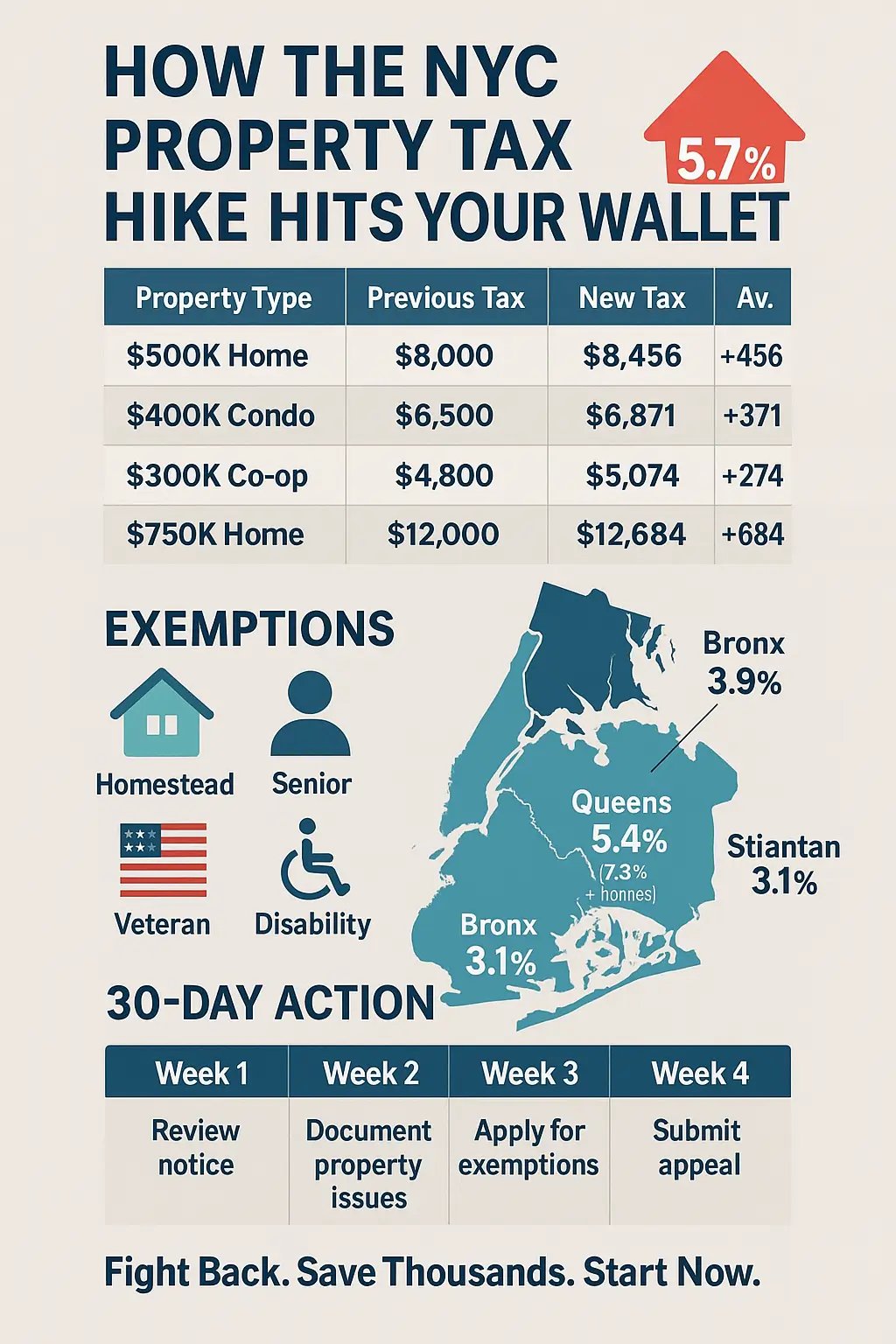

Visual Impact: What You'll Actually Pay

| Property Type | Previous Tax | After 5.7% Hike | Annual Increase |

|---|---|---|---|

| $500K Home | $8,000 | $8,456 | +$456 |

| $400K Condo | $6,500 | $6,871 | +$371 |

| $300K Co-op | $4,800 | $5,074 | +$274 |

| $750K Home | $12,000 | $12,684 | +$684 |

Single-Family Homeowners: The Hidden Tax on the American Dream

Class 1 properties (1-3 family homes) saw a 5.8% increase citywide, with Staten Island homeowners bearing the brunt at 7.8%.

For a typical homeowner with a $500,000 assessed value, this translates to an additional $1,450 to $1,950 annually in property taxes.

That's money that could have gone toward your child's college fund, emergency savings, or simply keeping your family's budget balanced.

Co-op and Condo Owners: The Steepest Climb

Class 2 properties (co-ops, condos, and rental buildings) experienced the harshest increase at 7.3%, with Brooklyn residents facing a brutal 9.4% jump.

If you own a $400,000 condo, you're looking at an additional $1,168 to $1,504 in annual taxes.

For many young professionals who stretched their budgets to afford their first home, this increase can feel like a betrayal of their financial planning.

Commercial Property Owners: The Ripple Effect

While Class 4 commercial properties saw a more moderate 3.8% increase, this still represents significant costs that often get passed down to tenants through higher rents.

This creates a cascading effect throughout the economy.

Borough-by-Borough Breakdown {#borough-by-borough-breakdown}

The NYC property tax assessment increase didn't hit all boroughs equally. Here's what homeowners in each borough face:

Brooklyn leads the pack with a 6.3% market value growth, meaning the highest property tax increases across the city.

Queens follows closely at 5.4%, with particular impact on co-op and condo owners.

Staten Island sits at 5.1%, but single-family homeowners face the steepest residential increases at 7.8%.

The Bronx experienced 3.9% growth, the most moderate among outer boroughs.

Manhattan had the smallest increase at 3.1%, but don't let this fool you. With property values already sky-high, even a 3.1% increase on a $2 million property means an additional $6,200 in annual taxes.

Hidden Costs of Higher Assessments {#hidden-costs-of-higher-assessments}

Beyond the obvious tax increases, NYC property tax hikes create hidden costs that can devastate family finances:

Escrow Account Shock

If you have a mortgage with an escrow account, your monthly payment will likely increase to cover the higher tax bill.

Many homeowners don't realize this until they receive their new payment schedule, creating immediate budget strain.

Refinancing Complications

Higher assessments can affect your loan-to-value ratio, potentially impacting your ability to refinance or obtain favorable terms on future loans.

Insurance Premium Increases

Property insurance rates often correlate with assessed values, meaning your insurance costs may also rise alongside your tax bill.

Opportunity Cost

Every dollar spent on higher property taxes is a dollar not invested in your family's future.

Whether that's retirement savings, education funding, or home improvements that could actually increase your property's value.

How the Assessment Process Works {#how-the-assessment-process-works}

Property assessment isn't magic, but it often feels that way to homeowners. Understanding the process gives you power to fight back effectively.

The Three Valuation Methods NYC Assessors Use

Market Approach: Assessors compare your property to similar homes that recently sold. This method works well for typical residential properties but can be problematic in unique neighborhoods or for distinctive properties.

Cost Approach: Used primarily for special-purpose properties, this method calculates replacement cost minus depreciation plus land value. It's less common for residential properties but understanding it helps you spot potential errors.

Income Approach: Applied to rental properties, this method analyzes potential rental income after expenses. If you own rental property, understanding this approach is crucial for successful appeals.

The Timing Game: When Your Assessment Gets Set

Your FY26 assessment reflects market activity from January 6, 2024, to January 5, 2025.

This timing gap creates opportunities and challenges. If your neighborhood has declined since the assessment period, you have grounds for appeal.

If it's improved significantly, you might face even higher assessments next year.

3-Phase Action Plan {#3-phase-action-plan}

After helping thousands of property owners navigate assessment challenges, I've developed a proven system for protecting your financial interests.

Phase 1: Immediate Assessment Review (Do This Now)

Step 1: Scrutinize Your Assessment Notice

Don't just look at the bottom line. Check every detail:

- Property dimensions and square footage

- Number of bedrooms and bathrooms

- Property classification

- Exemptions you should be receiving

- Comparable properties used in valuation

Step 2: Research Your Competition

Use online property databases to find similar properties in your area with lower assessments.

Document differences that justify your property having a lower value:

- Proximity to busy roads or commercial areas

- Property condition issues

- Less desirable lot characteristics

- Older systems or appliances

Step 3: Document Everything

Create a comprehensive file with:

- Photos of any property defects or needed repairs

- Repair estimates from licensed contractors

- Evidence of neighborhood issues (noise, safety concerns, etc.)

- Recent appraisals or inspections

Phase 2: The Property Tax Appeal Process (Your Legal Right)

Most property owners don't realize they have a fundamental right to challenge their NYC property tax assessment. Here's how to exercise that right effectively:

Understanding the Timeline

You typically have 30-60 days from receiving your assessment notice to file an appeal.

Missing this deadline often means waiting until the next assessment cycle, potentially costing you thousands in the meantime.

Building Your Case

Successful appeals require solid evidence. Based on my experience, these factors carry the most weight:

- Recent comparable sales showing lower values

- Professional appraisals supporting your position

- Documentation of property defects or needed repairs

- Evidence of neighborhood decline or negative factors

Professional vs. DIY Appeals

For modest increases on typical properties, you can often handle appeals yourself. However, consider professional help for:

- Properties with assessments over $750,000

- Commercial or investment properties

- Increases over 20%

- Properties with unique characteristics

Phase 3: Maximizing Your Exemptions (Free Money You're Missing)

Many property owners leave money on the table by not claiming available exemptions.

Exemptions You Might Be Missing {#exemptions-you-might-be-missing}

Homestead Exemptions: Most states offer property tax reductions for primary residences. In NYC, the Basic STAR exemption can save you hundreds annually.

Senior Citizen Exemptions: Property owners 65 and older often qualify for additional exemptions. Some programs can reduce assessed values by up to 50%.

Veteran Exemptions: Qualifying veterans, especially those with disabilities, may receive substantial property tax reductions or complete exemptions.

Disability Exemptions: Property owners with disabilities may qualify for significant assessment reductions.

Long-Term Protection Strategy {#long-term-protection-strategy}

Creating Your Tax Shock Absorber

The smartest property owners prepare for assessment increases before they happen:

Build a Tax Contingency Fund: Set aside 1-2% of your property's value annually in a dedicated savings account. This creates a buffer against unexpected increases.

Monitor Your Escrow Account: If you have a mortgage escrow account, review it quarterly and ask your lender to adjust withholdings if you anticipate tax increases.

Track Local Market Trends: Stay informed about development projects, zoning changes, and sales activity in your neighborhood. This knowledge helps you anticipate and prepare for assessment changes.

Strategic Property Improvements

While improving your property can increase its value, smart owners consider tax implications:

Focus on improvements that provide the best return on investment while minimizing assessment impact:

- Energy-efficient upgrades that may qualify for tax credits

- Curb appeal improvements like landscaping

- Interior updates that improve functionality without dramatically increasing square footage

Timing Matters: If major improvements are planned, consider timing them to minimize assessment impact. Avoid major renovations just before assessment periods when possible.

Real Owner Case Studies {#real-owner-case-studies}

Let me share some real examples (names changed for privacy) of how property owners have successfully navigated assessment challenges:

Maria's Story: A Staten Island homeowner faced a 12% assessment increase on her $450,000 home.

By documenting water damage in her basement and researching comparable properties, she successfully appealed and reduced her assessment by $35,000, saving $1,750 annually.

David's Challenge: A Brooklyn condo owner saw his assessment jump 18% despite no improvements to his unit.

He hired a property tax consultant who identified errors in the building's classification and secured a 15% reduction in his assessment.

Linda's Victory: A Queens senior citizen discovered she qualified for multiple exemptions she hadn't been receiving.

By applying for the Senior Citizen Homeowners' Exemption and Enhanced STAR, she reduced her annual tax bill by $2,400.

Tools and Resources {#tools-and-resources}

Modern property owners have access to powerful tools that level the playing field:

Property Assessment Websites: Use NYC Department of Finance's online tools to research comparable properties and track assessment history.

Tax Calculation Tools: Online calculators help estimate future bills based on different assessment scenarios.

Appeal Preparation Software: Digital tools help organize documentation and calculate potential savings.

Market Analysis Platforms: Real estate websites provide neighborhood trend data and comparable sales information.

30-Day Action Plan {#30-day-action-plan}

Don't let this information overwhelm you. Here's exactly what to do in the next 30 days:

Week 1: Review your assessment notice thoroughly and research comparable properties in your area.

Week 2: Document any property issues and gather evidence supporting a lower valuation.

Week 3: Apply for any exemptions you're eligible for but not currently receiving.

Week 4: If you decide to appeal, file your paperwork before the deadline.

Frequently Asked Questions {#faqs}

Q: How can I tell if my NYC property is over-assessed compared to similar properties?

A: Research comparable properties within a few blocks of your home that sold recently or have similar characteristics. If your assessment is significantly higher than similar properties, you may have grounds for appeal.

Look for properties with similar square footage, lot size, age, and condition. A difference of more than 5-10% in assessed value for truly comparable properties often justifies an appeal.

Q: What's the most effective way to document property defects for a NYC property tax appeal?

A: Create a comprehensive visual record with dated photographs showing any structural issues, outdated systems, or maintenance problems. Get written estimates from licensed contractors for major repairs.

Document environmental issues like noise, traffic, or unsightly neighboring properties. The key is showing how these factors would affect what a buyer would pay for your property compared to the "perfect" comparable properties assessors used.

Q: Can I appeal my NYC property tax assessment even if I recently bought the property?

A: Absolutely. Your recent purchase price can actually be powerful evidence in your favor if you paid less than the assessed value. However, be aware that if you paid more than the assessed value, this could work against you in future assessments.

The key is whether your purchase price reflects the property's true market value or if there were special circumstances affecting the sale.

Q: How do I know if hiring a professional property tax consultant is worth the cost?

A: Consider the potential savings versus the cost. Most consultants work on contingency, taking 25-50% of your first year's tax savings. If your potential savings exceed $1,000 annually, professional help often pays for itself.

This is especially true for commercial properties, high-value residential properties, or complex cases involving unique property characteristics.

Q: What happens if I miss the NYC property tax appeal deadline?

A: Missing the appeal deadline typically means waiting until the next assessment cycle, which could be 1-5 years depending on your jurisdiction. However, some areas allow late appeals under special circumstances like illness, military deployment, or if you can prove the assessment contains clear errors.

Contact your local assessor's office immediately to understand your options.

Q: How can I protect myself from future NYC property tax assessment shock?

A: Build a tax contingency fund by setting aside 1-2% of your property's value annually. Monitor local real estate trends and development projects that could affect your neighborhood. Stay informed about your assessment cycle and prepare documentation in advance.

Consider working with a property tax professional for ongoing monitoring if you own high-value or multiple properties.

Q: Are there any warning signs that my next NYC assessment might increase dramatically?

A: Yes, watch for these indicators: significant new construction in your area, major infrastructure improvements, nearby property sales at much higher prices than historical norms, neighborhood gentrification, or zoning changes that allow higher-density development.

If you see these signs, start preparing your appeal documentation and consider professional consultation.

Q: What's the difference between protesting an assessment and appealing a tax bill in NYC?

A: Protesting an assessment challenges the property's valuation, while appealing a tax bill typically involves challenging the tax rate or calculation. Most property owners should focus on assessment protests since this addresses the root cause of high taxes.

However, if you believe errors exist in how your taxes were calculated (such as missing exemptions), you may need to address both issues.

Q: Can improving my property actually hurt me tax-wise?

A: Major improvements can increase your assessed value, leading to higher taxes. However, the key is ensuring improvements add more value than they cost in additional taxes.

Focus on improvements that provide the best return on investment: energy efficiency upgrades, curb appeal enhancements, and functional improvements that don't dramatically increase square footage. Always factor potential tax increases into your renovation budget.

Q: How do I handle NYC property tax increases if I'm on a fixed income?

A: Explore these options immediately: apply for senior citizen exemptions if you're 65 or older, look into circuit breaker programs that cap taxes based on income, contact your tax collector about payment plans or hardship deferrals, and consider property tax deferral programs that let you pay accumulated taxes when you sell.

Don't wait until you're in crisis to explore these options.

Take Action Now: Protect Your Investment

NYC property tax assessment increases are a reality of property ownership, but they don't have to be a financial disaster. By understanding the process, knowing your rights, and taking proactive steps, you can protect your financial interests and potentially save thousands of dollars.

Remember, the assessment process isn't perfect, and you have every right to ensure you're paying your fair share, not more.

The key to success is action. Don't let frustration or intimidation keep you from fighting for what's fair. Start with the immediate steps outlined in this guide, and remember that every dollar you save on property taxes is a dollar that stays in your family's budget where it belongs.

Your property is likely your largest investment. The system may feel overwhelming, but you're not powerless. Armed with the right information and strategy, you can fight back—and win. Every dollar you save is one more invested in your family's future.

Take action now. Protect your home, your wallet, and your peace of mind.