From City Lights to County Life: The Ultimate First-Time Buyer's Guide to Rockland County

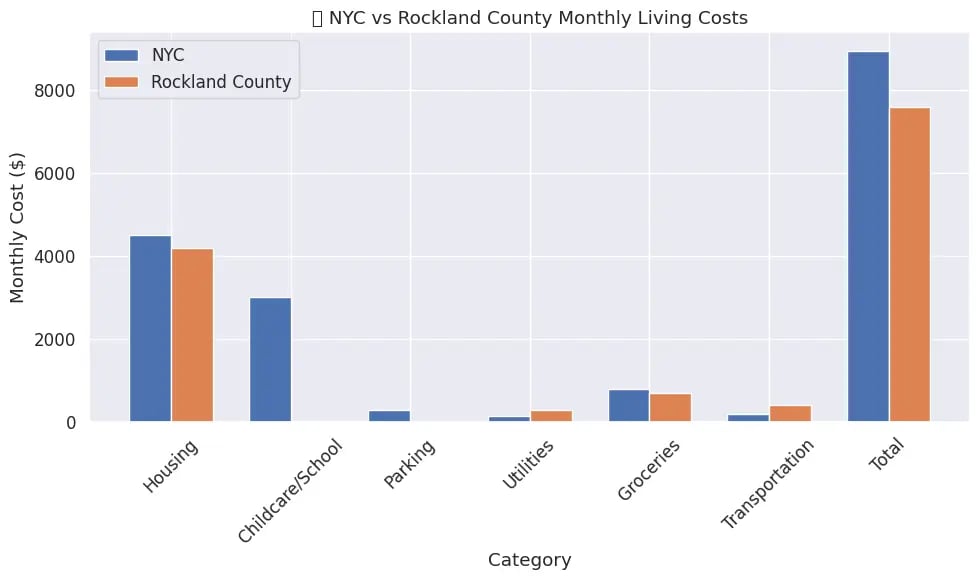

Picture this: You're cramped in a 400-square-foot Manhattan studio, paying $3,500 a month for the privilege of hearing your neighbor's conversations through paper-thin walls. Your friends with kids are juggling $2,000+ monthly daycare costs while dreaming of backyards. Sound familiar? You're not alone—and Rockland County might just be your answer.

The great NYC exodus isn't just a pandemic phenomenon; it's a lifestyle revolution. For first-time homebuyers, Rockland County represents something powerful: the chance to build real wealth through homeownership while maintaining that crucial connection to the city that shaped your career.

But here's what most guides won't tell you: moving from renter to homeowner, from city to suburbs, isn't just about finding a house—it's about completely reimagining your life. This comprehensive guide will walk you through every detail, from hidden costs to neighborhood secrets, ensuring your transition is not just successful, but transformative.

Why Rockland County Is NYC's Best-Kept Secret

The Numbers That Matter

Let's start with the reality check. Rockland County's median home price sits at approximately $679,000 as of 2025. Yes, that's significantly higher than the national average of around $420,000. But here's the perspective shift: in Manhattan, $679,000 might get you a one-bedroom co-op with monthly maintenance fees that could fund a vacation home elsewhere.

In Rockland County, that same investment typically gets you:

- 3-4 bedrooms with actual closet space

- A driveway (imagine that!)

- Property that appreciates over time instead of rent receipts

- Access to top-rated school districts

- Community amenities that would cost hundreds monthly in NYC

The Commuter's Paradise

The genius of Rockland County lies in its accessibility. The Tappan Zee Bridge (now Mario Cuomo Bridge) connects you to Westchester in 20 minutes. NJ Transit and Metro-North provide multiple routes into Manhattan. Many residents maintain hybrid work schedules, making the commute manageable while enjoying suburban benefits.

Pro Tip: Test your commute during actual work hours before buying. What looks like a 45-minute trip on Google Maps can become 90 minutes during peak times.

The Rockland County Neighborhood Deep Dive

Nyack: Where Artists and Families Collide (In the Best Way)

The Vibe: Think Brooklyn Heights meets Hudson Valley charm. Nyack pulses with creative energy while maintaining family-friendly suburban appeal.

The Real Estate Reality:

- Median home price: $750,000-$850,000

- Property types: Victorian homes, modern condos, riverfront properties

- Hidden gem: Condos starting around $400,000 for first-time buyers

Why Nyack Works for First-Timers:

- Walkable downtown means less car dependency

- Strong rental market if you need to relocate

- Active community events and cultural scene ease the suburban adjustment

- Excellent resale value due to unique character

The Nyack Challenge: Parking can be limited in the village center, and some older homes need significant updates.

New City: The Practical Choice That Doesn't Sacrifice Soul

The Vibe: Suburban functionality meets community spirit. It's where you'll find young professionals and growing families building their lives.

The Real Estate Reality:

- Median home price: $749,000

- New construction opportunities

- Planned affordable housing developments for qualified buyers

Why New City Wins:

- County seat benefits: better services, infrastructure

- New developments often include modern amenities

- Solid public transportation connections

- Growing commercial district

Insider Secret: New City's affordable housing initiatives can offer qualified first-time buyers homes starting around $300,000—but you need to act fast and meet strict income requirements.

Piermont: Small Town, Big Dreams

The Vibe: If Stars Hollow from Gilmore Girls existed in New York, it would be Piermont. Tight-knit community with stunning Hudson River views.

The Real Estate Reality:

- Higher price point: $800,000+ median

- Limited inventory creates competition

- Unique properties with character

The Piermont Payoff:

- Investment potential due to limited supply

- Waterfront lifestyle without Hamptons prices

- Strong community bonds and low crime rates

Clarkstown: Diversity Meets Suburban Comfort

The Neighborhoods Within: West Nyack, Bardonia, Congers, and New City all fall under Clarkstown's umbrella.

Why Clarkstown Works:

- Most diverse area in Rockland County

- Range of housing options and price points

- Excellent school districts across all areas

- Shopping and dining variety

First-Timer Advantage: Multiple neighborhoods mean various entry points into the market.

Sparkill and Tappan: The Hidden Gems

The Vibe: Quiet, family-focused communities where neighbors actually know each other's names.

The Appeal:

- Lower crime rates

- Excellent schools

- Commuter-friendly locations

Strong property value retention

The Real Pain Points (And How to Conquer Them)

Pain Point #1: The Down Payment Mountain

The Reality: After years of paying NYC rent, saving $135,000+ for a 20% down payment feels impossible.

The Strategy:

- 3% Down Programs: Many lenders offer first-time buyer programs requiring just 3% down

- Gift Money: Family contributions can cover down payment requirements

- Down Payment Assistance: Rockland Housing Action Coalition offers grants up to $50,000 for qualified buyers

- IRA Withdrawals: First-time buyers can withdraw up to $10,000 from IRAs penalty-free

Real Numbers Example: On a $675,000 home with 3% down, you need $20,250 plus closing costs (roughly $13,500), totaling around $35,000—still significant, but manageable compared to 20% down.

Pain Point #2: The Hidden Costs Shock

The Reality: Property taxes in Rockland County average 1.73% annually—among the highest in the nation.

Hidden Costs of Homeownership Breakdown

Monthly costs for a $675,000 Rockland County home:

| Cost Category | Monthly Amount | Annual Amount | Notes |

|---|---|---|---|

| Property Taxes | $973 | $11,673 | Based on 1.73% rate |

| Homeowner's Insurance | $100 | $1,200 | Standard coverage |

| PMI (if <20% down) | $250 | $3,000 | Removable at 20% equity |

| Utilities | $350 | $4,200 | Gas, electric, water, internet |

| Maintenance Reserve | $250 | $3,000 | 1% of home value annually |

| HOA/Condo Fees | $200* | $2,400* | *If applicable |

| Total Beyond Mortgage | $1,873-2,123 | $22,473-25,473 | Plan accordingly! |

The Strategy: Budget for $1,800-2,100/month in carrying costs beyond your mortgage payment.

Pain Point #3: The Mortgage Maze

The NYC Renter's Dilemma: Your NYC rental history means little to mortgage lenders focused on income ratios and credit scores.

The Solution Path:

- Clean Up Credit: Aim for 740+ credit score for best rates

- Document Everything: Stable employment history trumps high single-year earnings

- Consider Local Lenders: Rockland County banks understand the local market

- Get Multiple Quotes: Rates can vary significantly between lenders

Pain Point #4: The Bidding War Reality

The Truth: Even in a "neutral" market, desirable properties under $600,000 can trigger bidding wars.

Winning Strategies:

- Pre-approval Letter: Not pre-qualification—actual underwriting approval

- Escalation Clauses: Automatically increase your offer up to a specified limit

- Fast Closing: Offer 30-day or shorter closing periods

- Personal Letters: Connect with sellers emotionally (when appropriate)

- Inspection Contingency Strategy: Consider shortened inspection periods

Pain Point #5: The Suburban Adjustment Syndrome

The Challenge: Missing NYC's energy, convenience, and cultural diversity.

The Transition Strategy:

- Choose Walkable Areas: Nyack, Piermont village centers offer urban-like amenities

- Join Community Groups: Rockland County has active hiking clubs, book clubs, and professional networks

- Maintain City Connections: Plan regular NYC visits during your first year

- Embrace New Opportunities: Discover hiking trails, farmers markets, and community events impossible in NYC

Your Step-by-Step Roadmap to Homeownership

The Foundation Phase: Building Your Financial Fortress (3-4 Months)

Credit Score Mastery Your credit score is your golden ticket to better mortgage rates. A jump from 680 to 740 can save you $50,000+ over a 30-year loan. Start by paying down credit cards to below 30% utilization, but resist the urge to close old accounts—credit history length matters. Set up automatic payments to avoid late fees that devastate scores.

Credit Score Impact on Mortgage Rates

30-year fixed mortgage on $500,000 loan:

| Credit Score | Interest Rate | Monthly Payment | Total Interest Paid | Savings vs. 680 Score |

|---|---|---|---|---|

| 760+ | 6.5% | $3,160 | $637,600 | $54,000 |

| 740-759 | 6.7% | $3,210 | $655,600 | $36,000 |

| 720-739 | 6.9% | $3,280 | $680,800 | $10,800 |

| 700-719 | 7.1% | $3,340 | $702,400 | Reference |

| 680-699 | 7.3% | $3,410 | $727,600 | Baseline |

| <680 | 7.8%+ | $3,580+ | $788,800+ | -$61,200 |

Rates are illustrative and vary by lender and market conditions

The Savings Sprint Beyond your down payment, you'll need an emergency fund covering 6-12 months of total housing costs (mortgage, taxes, insurance, utilities). This typically means $15,000-25,000 for most Rockland County purchases. Open a high-yield savings account specifically for homebuying—keeping funds separate prevents accidental spending.

Document Detective Work Lenders want your financial life story. Create a "mortgage folder" with two years of tax returns, recent pay stubs, bank statements, and any asset documentation. Self-employed buyers need additional profit/loss statements and 1099s. The more organized you are, the faster your approval process.

Lender Shopping Strategy Don't just compare rates—compare total loan costs, closing fees, and service quality. Credit unions often offer competitive rates for first-time buyers, while larger banks may have more flexible programs. Get quotes within a 14-day window to minimize credit score impacts.

The Education Phase: Becoming a Market Expert (2-3 Months)

Neighborhood Intelligence Gathering Visit potential areas during rush hour, weekends, and evenings. Notice parking availability, noise levels, and how neighbors interact. Check crime statistics, future development plans, and local tax assessments. Subscribe to local Facebook groups and Nextdoor to understand community dynamics.

School District Deep Dive Even without children, school ratings dramatically affect property values and resale potential. Research not just overall district ratings but specific elementary school zones, as these vary within districts. Websites like GreatSchools.org provide detailed performance data and parent reviews.

Commute Reality Check Google Maps lies about rush hour times. Actually ride NJ Transit buses or trains during peak hours to experience real commute conditions. Factor in parking costs at train stations ($100-200/month) and weather delays. Test backup routes for when primary transportation fails.

Agent Matchmaking Interview multiple agents focusing on their recent first-time buyer experience, local market knowledge, and communication style. Ask for references from recent clients and verify their responsiveness. The right agent becomes your advocate, educator, and emotional support system.

The Hunt Phase: Finding Your Perfect Imperfect Home (2-4 Months)

The Non-Negotiables List Separate absolute needs from wishlist items. Non-negotiables might include: minimum bedrooms, parking, commute distance, or school district. Everything else becomes a trade-off. Remember, you can change paint colors and light fixtures—you can't change location or major structural elements.

Speed and Strategy In competitive markets, good properties disappear within days. Set up automatic MLS alerts and be ready to view homes within 24 hours of listing. Consider viewing homes virtually first to narrow options quickly. Have your pre-approval letter ready and know your maximum comfortable payment—not just what you qualify for.

Inspection Wisdom Never waive inspections entirely, even in bidding wars. Consider shortening inspection periods (5-7 days instead of 10) or limiting inspection objections to major issues only. Budget $400-600 for professional inspections, but remember—this small cost can save thousands in surprise repairs.

Negotiation Nuances Learn when to negotiate and when to pay full price. Overpriced properties offer negotiation opportunities, while fairly-priced homes in desirable areas may require full-price or above-asking offers. Consider non-price concessions like flexible closing dates or seller-paid closing costs.

The Victory Phase: Closing and Creating Home (Ongoing)

Pre-Closing Checklist Schedule your final walkthrough 24-48 hours before closing to ensure the property condition matches your contract. Verify all agreed-upon repairs are completed and no new damage has occurred. Arrange homeowner's insurance and transfer utilities at least one week before closing.

Closing Day Mastery Bring certified funds for down payment and closing costs—personal checks won't work for large amounts. Review all documents carefully, especially the mortgage terms and property deed. Don't hesitate to ask questions; this is your last chance to address concerns before signing.

First-Year Financial Planning Budget for immediate needs like moving costs, basic furnishings, and potential emergency repairs. Many new homeowners underestimate first-year expenses—plan for $5,000-10,000 in unexpected costs. Consider keeping some savings liquid rather than putting every dollar toward the down payment.

Community Connection Strategy Combat suburban isolation by actively joining local groups within your first 90 days. Attend town hall meetings, join neighborhood Facebook groups, or participate in community events. Many Rockland County towns have active hiking clubs, book clubs, and volunteer organizations that help newcomers build social connections.

Advanced Strategies for Success

The Investment Mindset

Think beyond your first home. Rockland County properties often become excellent rental investments when owners eventually upgrade. Consider:

- Basement Apartments: Many homes have separate entrances for rental income

- Accessory Dwelling Units: New zoning laws make these increasingly viable

- Location Appreciation: Properties near train stations and commercial areas appreciate faster

The Renovation Opportunity

Many first-time buyers dismiss homes needing work, but this can be your advantage:

- 203(k) Loans: Finance home purchase and renovations together

- Cosmetic vs. Structural: Learn to identify good bones vs. money pits

- Sweat Equity: DIY projects can build significant value over time

Comprehensive FAQ Section

Financial Questions

Q: What's the minimum income needed to buy a home in Rockland County? A: For a $675,000 home with 5% down, you'd need roughly $140,000 annual household income to qualify comfortably. However, debt-to-income ratios matter more than raw income—aim for total monthly debt payments under 36% of gross income.

Q: Are there specific first-time buyer programs in Rockland County? A: Yes, several options exist:

- Rockland Housing Action Coalition offers down payment assistance grants

- NYS SONYMA provides favorable mortgage terms for first-time buyers

- Local credit unions often have special first-time buyer programs

- Some employers offer homebuyer assistance programs

Q: How much should I save beyond the down payment? A: Plan for 2-3% of home price in closing costs, plus 3-6 months of housing expenses as an emergency fund. For a $675,000 home, budget $55,000-75,000 total cash needed.

Q: Can I use my 401(k) for a down payment? A: You can borrow up to 50% of your 401(k) balance (max $50,000) for a home purchase. Unlike withdrawals, loans don't trigger taxes or penalties if repaid properly.

Market and Timing Questions

Q: When's the best time to buy in Rockland County? A: Winter months (December-February) typically offer less competition and motivated sellers. However, inventory is also lower. Spring markets are competitive but offer more choices.

Q: How fast do homes sell in Rockland County? A: Average days on market varies by price point and condition. Well-priced homes under $600,000 often sell within 2-3 weeks, while higher-priced properties may take 60-90 days.

Q: Should I wait for prices to drop? A: Waiting for significant price drops while paying high rent often costs more than buying now. Focus on monthly payment affordability rather than timing the market perfectly.

Neighborhood and Lifestyle Questions

Q: Which neighborhoods have the best schools? A: Clarkstown Central, Nyack, and East Ramapo districts consistently rank highly. However, research specific schools within districts, as quality can vary by elementary school zones.

Q: How's the commute to Manhattan really? A: Expect 60-90 minutes door-to-door during peak hours. NJ Transit buses from Rockland are often faster than trains. Consider reverse commuting to New Jersey for potentially shorter trips.

Q: What about diversity and community? A: Clarkstown areas offer the most diversity. Nyack has a strong arts community. Many neighborhoods host cultural festivals and community events throughout the year.

Q: Are there good restaurants and nightlife? A: Nyack offers the most dining and nightlife options. New City and West Nyack have growing restaurant scenes. Most areas are family-focused rather than nightlife-centric.

Process and Logistics Questions

Q: How do I find a good real estate agent? A: Look for agents with:

- 5+ years local experience

- Recent first-time buyer clients

- Strong knowledge of financing options

- Availability for weekend showings

- Positive reviews from recent clients

Q: What should I look for during home inspections? A: Beyond obvious issues, focus on:

- Electrical system age and capacity

- HVAC system condition

- Roof age and condition

- Foundation and basement moisture

- Water pressure and plumbing

- Insulation and energy efficiency

Q: How negotiable are prices in Rockland County? A: Negotiation success depends on market conditions, property condition, and time on market. Well-priced homes may receive multiple offers, while overpriced properties offer negotiation opportunities.

Q: What are closing costs, and who pays what? A: Typical buyer closing costs include:

- Mortgage origination fees (1-2% of loan)

- Appraisal ($500-800)

- Title insurance ($1,000-2,000)

- Attorney fees ($1,500-3,000)

- Property taxes and insurance escrow

- Home inspection ($400-600)

Long-term Planning Questions

Q: How's the resale market for first-time buyer homes? A: Starter homes in good school districts maintain strong resale value. Properties under $600,000 typically have the broadest buyer pool when it's time to sell.

Q: Should I consider a condo or single-family home? A: Condos offer:

- Lower maintenance responsibilities

- Often lower price points

- Shared amenities

- HOA fees (budget $200-500/month)

Single-family homes offer:

- More privacy and space

- No HOA restrictions

- Potential for additions/modifications

- Generally better appreciation

Q: What if I need to move back to NYC? A: Many Rockland County properties make excellent rental investments. Research rental market rates in your target neighborhoods before buying.

🏡 Ready to Make Your Move? Let's Talk Strategy!

Thinking of buying your first home in Rockland County? You don't have to navigate this alone. Our local experts have helped over 150 NYC families successfully make the transition from renter to homeowner.

What You Get:

✅ Personalized Market Analysis - See exactly what you can afford in your preferred neighborhoods

✅ Hidden Cost Calculator - No surprises on closing day

✅ Pre-Approved Lender Network - Skip the mortgage maze with our trusted partners

✅ Exclusive Off-Market Listings - Access properties before they hit the MLS

📞 [Schedule Your Free 30-Minute Strategy Call]

No pressure, just expert guidance tailored to your NYC-to-suburbs journey🏠 Your Journey Starts Here - Let's Make It Happen