Picture this: You're scrolling through rental listings in New York City, feeling that familiar pang of frustration as you watch your monthly rent payments disappear into your landlord's pocket. Then you stumble across something intriguing: a "rent-to-own" listing promising you can work toward homeownership while you rent. Sounds like the perfect solution, right?

Hold on. Before you get swept away by the promise of finally owning a piece of the Big Apple, there's a lot you need to know about rent-to-own arrangements in NYC. As someone who has spent years navigating New York's complex real estate landscape, I can tell you that while these deals might sound appealing on the surface, they're fraught with complications that could cost you thousands of dollars and years of financial setback.

TL;DR: Key Takeaways

- Rent-to-own NYC deals are extremely risky - regulatory warnings, predatory terms, and financial traps abound

- You'll likely pay $25,000+ more than regular rent over 3 years with minimal equity building

- Better alternatives exist - NYC Housing Connect, HomeFirst DPA, and FHA loans offer safer paths

- If you must consider it - hire a lawyer, get independent inspections, and verify property ownership first

In this comprehensive guide, I'll walk you through everything you need to know about rent-to-own homes NYC, share real insights from my experience in the market, and most importantly, show you better alternatives that can actually help you achieve your homeownership dreams safely and affordably.

What Exactly Are Rent-to-Own NYC Agreements?

Let's start with the basics. A rent-to-own agreement is essentially a hybrid arrangement that combines renting with a future purchase option. You rent a property for a predetermined period (usually 1-3 years) with either the option or obligation to buy it at the end of the lease term.

These agreements typically include several key components:

The Lease Agreement: This looks like your standard rental lease, outlining monthly rent, lease duration, and tenant responsibilities. However, the monthly rent is usually higher than market rate because a portion goes toward your future down payment.

The Purchase Agreement: This document sets the purchase price (often determined upfront), the timeline for exercising your purchase option, and the specific conditions you must meet to complete the sale.

The Option Fee: This is a non-refundable upfront payment, typically ranging from $3,000 to $15,000 in NYC, that gives you the exclusive right to purchase the property. Think of it as "buying" the option to buy.

Rent Credits: A portion of your monthly rent (usually 10-25%) gets credited toward your eventual down payment or closing costs, assuming you complete the purchase.

The Two Main Types of Rent-to-Own Deals

Understanding the difference between these two types could save you from legal and financial disaster:

Lease-Option Contracts: The "Maybe" Agreement

With a lease-option, you have the choice to buy or walk away at the end of the lease term. If you decide not to purchase (maybe you found issues with the property, or your financial situation changed), you're not legally obligated to buy. However, you'll lose your option fee and any rent credits you've accumulated.

Real-world example: Sarah paid a $5,000 option fee and $200 monthly rent credits over two years on a Brooklyn apartment. When she discovered major structural issues during her final walk-through, she chose not to purchase. She lost $9,800 ($5,000 + $4,800 in rent credits) but avoided buying a problematic property.

Lease-Purchase Contracts: The "Must Buy" Agreement

This is where things get dangerous. With a lease-purchase agreement, you're legally obligated to buy the property at the end of the lease term. If you can't secure financing, your circumstances change, or you simply change your mind, you could face legal action and lose everything you've paid.

Why this matters: In NYC's volatile real estate market, your financial situation can change dramatically in 2-3 years. Job loss, medical emergencies, or market crashes could make it impossible to complete the purchase, leaving you liable for breach of contract.

The Harsh Reality: Why Lease-to-Own NYC Deals Rarely Work

After analyzing dozens of rent-to-own cases in NYC over the past decade, I can tell you why these deals are so problematic in our market:

1. New York's Regulatory Landscape is Hostile to These Deals

The New York Department of Financial Services has been actively investigating rent-to-own companies, with many arrangements potentially violating state lending and housing laws. According to the DFS consumer advisory, these agreements may impose harsh terms with little or no safeguards.

DFS Warning: "These agreements may impose harsh terms with little or no safeguards" - NY Dept. of Financial Services, 2024 advisory.

When regulators are this concerned, it's a red flag that should make you think twice.

The issue is that many rent-to-own agreements blur the line between renting and lending, potentially subjecting them to mortgage regulations without providing borrower protections. This puts you in a legal gray area where you might not have tenant rights or homeowner protections.

2. The Numbers Simply Don't Add Up for Rent-to-Own Apartments NYC

Let's talk real numbers. As of May 2025, NYC's median home value sits at $796,665 according to Zillow.com, with Manhattan properties averaging $1.39 million per Redfin.com data.

Here's what the financial reality looks like:

| Item | Rent-to-Own Deal | Regular Rent |

|---|---|---|

| Monthly payment | $4,500 | $3,800 |

| Extra "premium" | +$700 | - |

| Rent credits | $450 | n/a |

| Net outflow (36 mo) | $192,200 | $136,800 |

| Net equity after 3 yr | $31,200* | $0 |

*Assuming you complete the purchase and don't lose credits

You're essentially financing your own down payment at an astronomical interest rate. Over three years, you've paid $55,400 more than market rent just to accumulate $31,200 in credits.

3. Co-op Complications Make Things Worse

About 75% of NYC apartments are co-ops, which adds another layer of complications. Co-op boards have strict financial requirements and approval processes. Even if you complete your rent-to-own agreement successfully, there's no guarantee the co-op board will approve your purchase application.

I've seen situations where buyers lost their entire investment because they couldn't get co-op approval, even though they met all the rent-to-own contract requirements.

4. Property Condition Nightmares

Here's something most people don't realize: many rent-to-own properties are offered because they have serious issues that make them difficult to sell through traditional channels. These might include:

- Code violations that require expensive repairs

- Structural problems that aren't immediately apparent

- Properties facing potential demolition or major assessments

- Units with title issues or legal complications

The worst part? Most rent-to-own agreements don't allow for independent inspections or appraisals, so you're buying blind.

NYC Rent-to-Own Scams and Red Flags to Avoid

Unfortunately, the rent-to-own space attracts its share of fraudsters. Here are the warning signs I tell all my clients to watch for:

Classic Scam Tactics

The Fake Owner Scam: Someone advertises a property they don't own, collects your option fee and first month's rent, then disappears. Always verify ownership through public records before paying anything.

The Too-Good-To-Be-True Deal: A beautiful Manhattan apartment offered for $2,000/month rent-to-own? It's probably a scam. If it seems unrealistic for the market, it probably is.

Wire Transfer Demands: Legitimate transactions don't require wire transfers or cryptocurrency payments. Scammers love these untraceable payment methods.

Pressure Tactics: Any seller who demands immediate payment or won't let you review documents with an attorney is likely running a scam.

Protecting Yourself

- Always tour the property in person before paying anything

- Verify the seller's identity and ownership through city records

- Use secure payment methods with buyer protections

- Never send money based solely on online photos or virtual tours

- Report suspicious listings to local authorities and platforms immediately

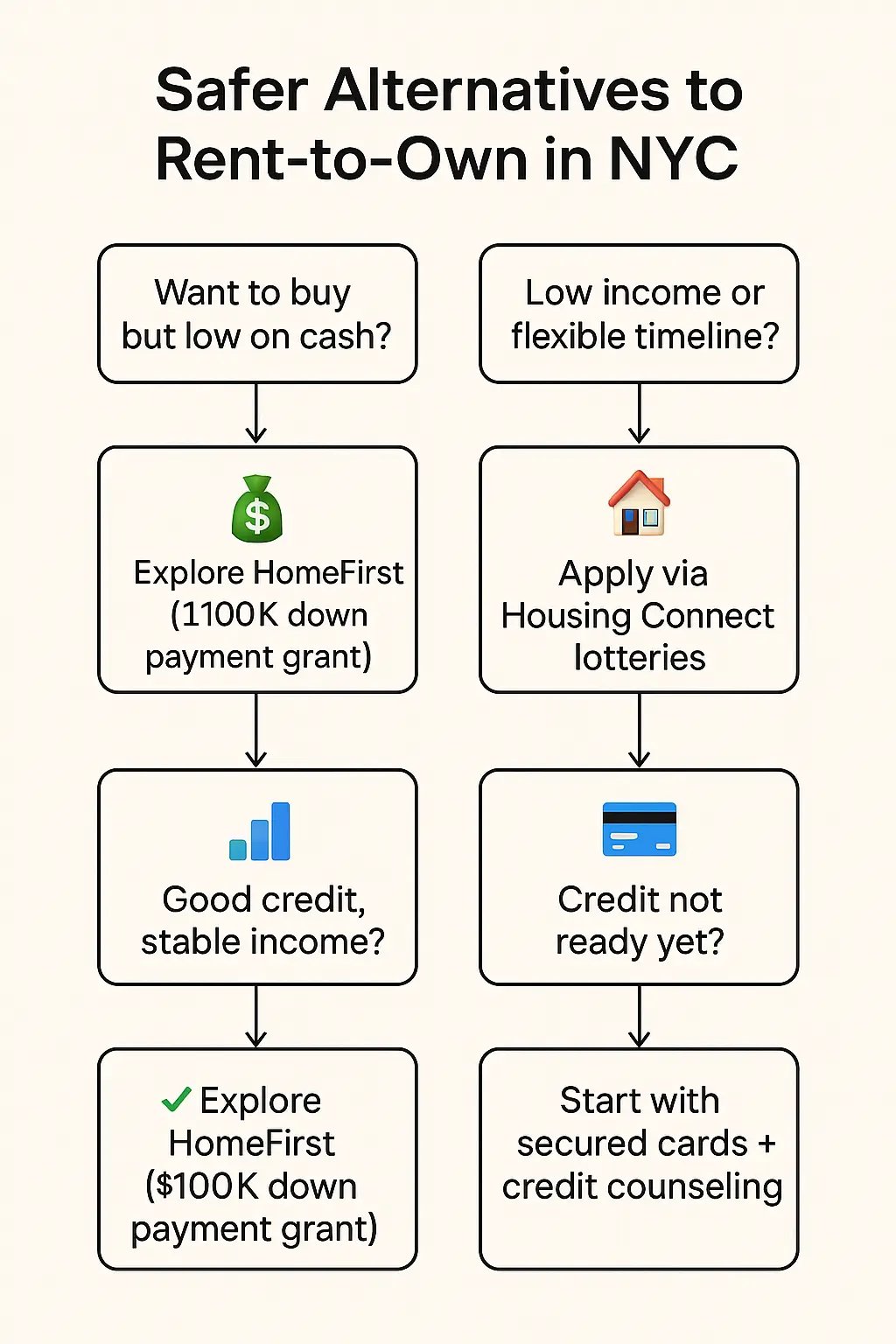

Smart Alternatives: Your Quick-Start Roadmap to NYC Homeownership

Instead of risking your financial future on a questionable rent-to-own deal, follow this proven 4-step roadmap:

Step 1: Check Your Credit (Free)

Get your free annual credit report at annualcreditreport.com. Know your score and identify areas for improvement.

Step 2: Open a High-Yield Down Payment Fund

Set up automatic transfers to a dedicated savings account. Even $200/month adds up to $7,200 annually.

Step 3: Apply Broadly on Housing Connect

Aim for 10+ lotteries at housingconnect.nyc.gov. It's free and your best shot at affordable homeownership.

Step 4: Get Professional Guidance

Book a consultation with a HUD-approved housing counselor for personalized strategy.

Snapshot of NYC Assistance Programs

Don't navigate this alone. These programs offer real money with transparent terms:

- HomeFirst DPA - Up to $100,000 forgivable for first-time buyers (≤80% AMI)

- CityLIFT - $30,000 forgivable in Bronx/Brooklyn after 5 years residence

- SONYMA - Below-market interest rates for qualified buyers statewide

- Housing Connect - Lottery system for affordable co-ops and condos citywide

Expert Tip: These programs have waiting lists, but they're legitimate opportunities with consumer protections that rent-to-own deals lack.

NYC's Official Affordable Housing Programs

NYC Housing Connect is the city's official platform for affordable housing opportunities.

This isn't some fly-by-night operation; it's run by the city with proper oversight and consumer protections. The platform offers:

- Transparent lottery systems for affordable rentals and purchases

- No broker fees or application costs

- Properties across all five boroughs

- Clear income requirements and application processes

I've helped numerous clients successfully navigate Housing Connect, and the key is persistence. Apply for multiple lotteries and be patient; the wait is worth it for the security and savings.

Down Payment Assistance Programs That Deliver

HomeFirst Down Payment Assistance Program: This program provides qualified first-time homebuyers with up to $100,000 toward down payment or closing costs. The income limits are reasonable, ranging from $130,440 for single-person households to $246,000 for eight-person households.

CityLIFT Program: Offers up to $30,000 in down payment assistance for eligible buyers in The Bronx or Brooklyn. The best part? The funds are fully forgivable after five years of residence.

These programs provide real money with clear terms and proper legal protections, unlike the murky world of rent-to-own deals.

Traditional Mortgage Options: Rent-to-Own vs FHA Loan NYC

Don't overlook conventional financing. Here's how traditional options stack up against rent-to-own:

- FHA loans with as little as 3.5% down

- VA loans for eligible veterans with zero down payment

- USDA loans for qualifying areas

- First-time homebuyer programs with reduced rates and fees

| Factor | Rent-to-Own | FHA Loan |

|---|---|---|

| Down payment | 15-20% (via credits) | 3.5% |

| Monthly cost | $700+ premium | Market rate |

| Legal protections | Minimal | Full federal backing |

| Financing certainty | Uncertain until closing | Pre-approved rates |

| Total cost (3 years) | $55,400+ extra | Standard mortgage payments |

When Rent-to-Own NYC Might Actually Make Sense

I'd be remiss if I didn't acknowledge that there are rare situations where rent-to-own could work, but they require very specific circumstances:

The Ideal Candidate Profile

You might consider rent-to-own if you meet ALL of these criteria:

- High, stable income with excellent job security

- Excellent credit score (750+) with minor issues that will resolve in 1-2 years

- Substantial savings already accumulated

- Strong understanding of real estate and contract law

- Access to qualified legal representation

- The property is being offered by the actual owner (not a rent-to-own company)

- You've had the property independently inspected and appraised

- The rent credits and terms are genuinely favorable

Even then, I'd strongly recommend exploring traditional alternatives first.

Expert Tip: If you meet all these criteria, you probably qualify for traditional financing with better terms and protections.

Questions to Ask Before Considering Any Rent-to-Own Deal

If you're still considering this route despite all the warnings, here are the critical questions you must ask:

- Can I have the property independently inspected and appraised?

- What happens if I lose my job or face a medical emergency?

- Are the rent credits guaranteed even if property values decline?

- What specific financing do I need to qualify for, and what if rates increase?

- Can I review all contracts with my attorney before signing?

If you get evasive answers to any of these questions, walk away immediately.

The Legal Protection Gap

One of the most concerning aspects of rent-to-own arrangements is the legal gray area they occupy. As a tenant, you're protected by New York's strong tenant protection laws. As a homebuyer, you're protected by various consumer protection and lending regulations. But rent-to-own agreements often fall between these protections, leaving you vulnerable.

New York's tenant protections include:

- Right to safe and habitable housing

- Protection from harassment and illegal eviction

- Anti-discrimination protections

- Rent stabilization laws in many cases

These protections typically don't apply to rent-to-own arrangements, so you could find yourself without recourse if problems arise.

My Professional Recommendation

After years of experience in NYC real estate and seeing the aftermath of failed rent-to-own deals, my advice is simple: avoid them. The risks far outweigh any potential benefits, especially in New York's complex and expensive market.

Instead, focus your energy on:

- Building your credit score through responsible financial management

- Saving for a down payment using high-yield savings accounts or CDs

- Exploring legitimate assistance programs like those offered by NYC and New York State

- Working with qualified professionals who can guide you through traditional homebuying processes

Comprehensive FAQ Section

General Questions

Q: Are rent-to-own agreements completely illegal in New York? A: They're not explicitly illegal, but New York's Department of Financial Services is actively investigating whether many of these arrangements violate state lending and housing laws. The regulatory uncertainty alone should give you pause.

Q: How much money do I typically need upfront for a rent-to-own agreement in NYC? A: Option fees typically range from $5,000 to $25,000, depending on the property value. You'll also pay above-market rent monthly. For a $800,000 property, expect to pay $12,000-$24,000 upfront plus $300-$600 extra monthly in rent. Based on current market data from Zillow.com showing median NYC home values at $796,665, these costs can be substantial.

Q: What happens if I can't get financing at the end of the lease term? A: With lease-option agreements, you lose your option fee and rent credits but aren't legally obligated to purchase. With lease-purchase agreements, you could face legal action and be liable for the seller's damages, potentially costing you tens of thousands more.

Q: Can I get pre-approved for a mortgage during the rental period? A: Most lenders won't provide final approval until you're ready to close, meaning interest rates could change significantly. Some lenders offer conditional pre-approval, but rates and terms aren't locked in.

Financial Questions

Q: Are rent credits guaranteed if property values decline? A: This depends entirely on your contract terms. Many agreements don't protect you if property values drop, meaning you could be obligated to buy a property for more than it's worth.

Q: How do NYC's high property values affect the math on rent-to-own deals? A: The high values make these deals extremely expensive and often uneconomical. When option fees alone can be $15,000-$25,000, and you're paying $500-$1,000 extra monthly in rent, the total cost often exceeds what you'd pay through traditional financing.

Q: What tax implications should I consider? A: Rent payments typically aren't tax-deductible like mortgage interest. Consult a tax professional, but don't expect the tax benefits of homeownership until you actually own the property.

Legal and Practical Questions

Q: Should I hire a lawyer for a rent-to-own agreement? A: Absolutely. Given the complexity and potential legal issues, having an attorney review any rent-to-own agreement is essential. The multiple contracts involved require careful legal scrutiny, and the cost of legal review is minimal compared to potential losses.

Q: Do I have tenant rights in a rent-to-own agreement? A: This is unclear and varies by agreement. Many rent-to-own arrangements exist in a legal gray area, potentially lacking both tenant protections and homeowner rights. You could find yourself without the protections of either.

Q: What should I look for in a legitimate rent-to-own agreement? A: Legitimate agreements should include clear purchase terms, fair rent credits, property inspection rights, proper legal documentation, and transparent financial terms. Avoid any deal that restricts inspections or has unclear terms.

Q: How can I verify that the seller actually owns the property? A: Check public records through the NYC Department of Finance's ACRIS database (Automated City Register Information System). You can search property records online to verify ownership. Never proceed without confirming ownership.

Alternatives and Better Options

Q: What are the best alternatives to rent-to-own in NYC? A: Focus on NYC Housing Connect for affordable housing lotteries, down payment assistance programs like HomeFirst and CityLIFT, traditional FHA loans, VA loans if you're eligible, and first-time homebuyer programs offered by various lenders.

Q: How long does it typically take to save for a down payment in NYC? A: This varies greatly by income and property price, but most financial advisors recommend saving 10-20% of the purchase price. For a $800,000 property, that's $80,000-$160,000, which could take 3-7 years of dedicated saving for most households.

Q: Are there any legitimate rent-to-own companies operating in NYC? A: While some companies claim to operate legitimately, the regulatory uncertainty and high risk make it difficult to recommend any. Focus on regulated programs and traditional financing instead.

Q: What if I have bad credit but want to work toward homeownership? A: Focus on credit repair first. Work with a non-profit credit counseling service, pay down existing debts, and consider secured credit cards to rebuild your score. Many first-time buyer programs accept lower credit scores than conventional loans.

Final Thoughts

The dream of homeownership in New York City is challenging enough without adding the unnecessary risks and complications of rent-to-own arrangements. While these deals might seem like a shortcut to homeownership, they're more often a detour that leads to financial loss and legal complications.

Your path to homeownership in NYC should be built on solid ground: good credit, adequate savings, proper financing, and professional guidance. It might take longer than a rent-to-own arrangement promises, but you'll end up with actual ownership, legal protections, and financial security.

Remember, if something sounds too good to be true in New York's real estate market, it probably is. Stick with proven, regulated programs that have helped thousands of New Yorkers achieve sustainable homeownership. Your future self will thank you for choosing the safer, more reliable path.

The information in this guide is based on current market conditions and regulations as of June 2025. Real estate laws and market conditions can change. Always consult with qualified legal and financial professionals before making any major real estate decisions.